BUILDER ECONOMICS IN HIP-3: IS DEPLOYING PERPETUALS STILL WORTH IT?

An incentive and sustainability analysis of deploying perpetual markets on Hyperliquid.

INTRODUCTION

Hyperliquid has just introduced its newest improvement proposal, HIP-4, which enables prediction market/outcome trading, illustrating a strategic shift beyond perpetual (perp) futures into broader derivatives primitives.

Yet, this evolution also naturally leads to some questions about the potential of HIP-3, which supports permissionless builder-deployed perps. While HIP-3 promised a new “open marketplace” where builders could earn fees and bootstrap their own perps, the actual economics observed on-chain raise an important question:

Is deploying a HIP-3 perp still attractive for builders today?

This article is to evaluate the current and future economics of HIP-3 builders, quantify the revenue potential against operational and structural drawbacks, and assess whether listing perp markets on HL remains a worthwhile strategy in the evolving competitive landscape.

KEY TAKEAWAYS

This article will analyze the feasibility of HIP-3 in the deployer perspective through the following main sections:

Section 1: Understanding about HIP-3 deployment

Section 2: Analyze the economic feasibility of HIP-3 based on the current performance through the estimated revenue and RoSC indicator; along with the reasons behind the current dominance of TradeXYZ.

Section 3: Identify some potential purposes as well as criteria that a builder often care about listing a perp DEX on HIP-3 under the non-financial perspective.

Section 4: A forward-looking vision of the paths that subsequent builders might choose to deploy on HIP-3.

SECTION 1: HIP-3 DEPLOYMENT OVERVIEW

Before HIP-3, listing new perp markets is mainly controlled by Hyperliquid’s core team, which is similar to that of a traditional centralized exchange (CEX) like Binance, and delistings are driven by validator votes.

This approach seems to go against the core values of a decentralized exchange like HL. Therefore, in October 2025, HIP-3 was introduced to allow any builders to deploy a perp DEX on HL’s infrastructure without permission. Since the launch of this proposal, in addition to validator-operated perps, HL now has another type of market called builder-deployed perps.

With the participation of TradeXYZ, the first builder-deployed market on HIP-3 as well as the first equity perp market on HL, HIP-3 is gradually seeing more entries from other builders, such as Felix, Ventuals, HyENA, KM, DreamCash and ABCDEx (coming soon).

After over 3 months of launch, this market is about to approach $40B in the cumulative trading volume, accounting for roughly 1% the all-time trading volume of HL. TradeXYZ market is still dominating at nearly 90% as reflected in the picture below.

1/ HIP-3 Deployer’s Responsibilities

Listing a perp market on HIP-3 is not simply a listing process, but a full market deployment lifecycle.

Unlike the centralized listing market model, HIP-3 requires builders to handle everything from designing specs to monitoring performance, making HIP-3 a system which is not only open but also places builders in a more specialized role.

The deployer of a perp market is responsible for: market definition and market operation.

Market definition (Step 1-4)

Step 1:

In order to deploy a perp DEX on HL, each builder is required to stake at least 500k $HYPE, currently valued at around $15M, which will be locked for at least 30 days. Unlike ETH staking on Ethereum, this stake amount is not used for consensus assurance or block reward earning. Instead, it acts as a performance guarantee, where deployers may lose their stake if their market operations are not good (explained later).

Step 2+3:

After meeting the staking requirement, the builder can deploy one perp DEX and design it by themselves, with its own underlying assets, collateral (i.e. USDH, USDT), order book system, and other independent contract configurations, including setting oracle prices, leverage limits, and settling the market (if needed).

Step 4:

The first 3 assets (i.e. BTC/USDH, ETH/USDH) in any perp DEX can be deployed directly, while additional markets (i.e. TSLA/USDH, NVDIA/USDH) require going through a Dutch auction, whose each round lasts 31 hours, the starting price each time is double the previous final price.

This mechanism is like an economic filter to prevent random listing or spam markets, which can lead to fragmented liquidity. In short, only assets that are expected to generate significant trading activity are worth the initial auction cost.

Once the market goes live, the builder is ready to operate it (Step 5).

Market operation (Step 5)

After the market is deployed, builders do not interfere with order book system but responsible for market correctness, including oracle system, price verification and risk monitoring.

Like validator-operated perps, HIP-3 perp DEX is operated on-chain and transparently. Therefore, every deployer input can be analyzed by validators. If input is considered irregular, causing downtime/invalid state or making any malicious/incompetent behavior, validators can vote slash stake (up to 100%).

Because builders need to commit a significant stake value while may face the risk of slashing, deployment is not a low-cost investment decision but quite a risky one. This can be understood that HIP-3 is not just about “deployment,” but about transferring risk and market design decisions from the protocol to the builder.

Therefore, understanding the balance between potential benefits and the risk of HIP-3 deployment becomes extremely important.

2/ HIP-3 Deployer’s Benefits and Risks

Under HIP-3, builders can inherit the HyperCore infrastructure including its high performance margining and order books. For example, the API to trade HIP-3 perps is unified with other HyperCore actions.

Above all, listing a perp DEX on HIP-3 comes with the right of receiving half of fee revenue from market performance (fee share is fixed at 50%).

However, as mentioned above, any builders accused of malicious/incompetent behaviors can get slashed by conducting a stake-weighted validator vote (up to 100%), meaning losing all 500k $HYPE staked amount. Even if the deployer has begun withdrawing stakes, the stake is still slashable during the 7-day waiting period.

That’s why HIP-3 deployer is not only a market operator but also must maintain its risk management role.

Though this model offers builders certain flexibility and ownership to their perp products, it also creates a trade-off between capital commitment, operational responsibility, and potential financial returns. To assess whether this trade-off is justified, the following section will examine the financial feasibility of implementing the HIP-3 project from the builder’s perspective.

SECTION 2: FINANCIAL PERSPECTIVE - IS DEPLOYING A HIP-3 PERP STILL FINANCIALLY ATTRACTIVE FOR BUILDERS TODAY?

From a builder perspective, revenue is the first thing to consider when it comes to building a perp DEX, on HIP-3, in this case.

So, is deploying a HIP-3 perp still financially attractive for builders today?

In order to answer this question, we need to consider two main factors: estimated revenue and Return on Staked Capital (RoSC).

And it’s important to note that, though transaction volume and fees generated primarily come from the underlying products and partner protocols, HIP-3 serves as a critical infrastructure enabling these products to be deployed, scaled, and monetized within HL.

Therefore, the performance metrics analyzed below should be understood as results achieved through HIP-3, not independently of it.

1/ Estimated Revenue

NOTE: In order to work out the estimated revenue, we also collected some figure from Hyperzap, and assume that:

Each deployer’s oracle performance is stable

The price of $HYPE is at $30

There’s no prolonged depegging of the quote asset

Revenue sources mainly come from the trading fee and staking yield

In reality, HIP-3 revenue is also dependent on market growth and sensitive to liquidation dynamics.

Here’s the formula:

For a more accurate simulation, we will choose projects that’s been launched for at least one month. Currently there are 4 main partners on the HIP-3 market, including TradeXYZ, Felix, Ventuals and HyENA. Besides, some remaining builders like KM (markets by Kinetiq) and DreamCash have also joined but we will not consider the performance of these 2 markets as they’re only launched 3 weeks ago.

TradeXYZ, the earliest deployer launched 3 months ago, is sharing nearly 90% trading volume of the whole HIP-3 market, enabling trading with major equity products like XYZ100 (NASDAQ100), TSLA, NVDA, or GOOGL.

According to Hyperzap:

The cumulative trading fee that TradeXYZ has collected is about $3.34M in 3 months, so on average, its monthly collected fee is over $900k.

However, according to Hyperliquid HIP-3 docs, from the deployer perspective, the fee share is fixed at 50%. So, the adjusted trading fee that TradeXYZ collected in practice is over $450k.

Together with the $HYPE staking yield (~ $30k), XYZ market’s monthly revenue is over $480k.

As such, we estimate that this market will gain over $5.8M in the yearly revenue. Based on this figure, TradeXYZ’s payback time will be less than 3 years.

Applying the same methodology, HyENA and Felix, launched nearly 2 months ago, are ranked second and third, and ranked last by Ventuals with the super small trading volume and fee as our metrics above. Specifically:

HyENA:$1.6M/year payback period of over 9 years

Felix: $950k/year payback period of over 15 years

Ventuals: $450k/year payback period of over 30 years

At these levels, achieving capital recovery appears highly challenging for crypto projects operating under current market conditions.

2/ Return On Staked Capital (RoSC)

Because HIP-3 requires capital to be locked up rather than spent, the crucial question for the deployer is not capital recovery, but capital yield. And we decide to use the Return on Staked Capital (RoSC) indicator, which is quite the same as Return on Investment (ROI), a financial ratio used to measure the benefit an investor receives in relation to their investment cost. But in this case, Staked Capital is not lost from the start.

RoSC is used to answer the question: “With the same 500k HYPE locked (~$15M), is deploying HIP-3 more worthwhile than not deploying at all?” In simple terms, RoSC stated how effectively each USD of $HYPE staked is “working“.

Below is the formula of RoSC:

Where:

Annual Fee Revenue: the estimated fee income per year as calculated above

Staked $HYPE value: the value of staked $HYPE as calculated above

Our goal is to compare the fee returns of deploying a perp DEX on HIP-3 with other investment strategies with the same amount of money (~15M).

If not deploying a perp DEX on HL, this capital could be allocated to other yield strategies across DeFi.

Currently, the staking APY of HYPE is only around 2.26%. The supply yield on some popular DeFi lending protocols like AAVE or Compound is often around 4%.

By CAIA, ETH staking yields are around 2–4% depending on the protocol and chain, while SOL staking yields are around 6–7%.

However, CoinDesk stated that lending or restaking strategies sometimes achieve returns of 10–25% in environments that encourage incentives.

So, we believe that:

If RoSC < 5%, deploying on HIP-3 is financially ineffective (Red)

If RoSC 5-10%, deploying on HIP-3 is strategic (Yellow)

If RoSC > 10%, deploying on HIP-3 is highly profitable (Green)

Based on the above formula and these assumptions, below is our result of every market.

NOTE: These assumptions are not meant to be precise forecasts, but rather a reasonable baseline for comparative analysis.

Our result shows that RoSC of TradeXYZ is over 36% (Green), followed by HyENA at 8.6% (Yellow) and Felix at 4.05% (Red), whereas the remaining market (Ventuals) is only 0.78% (Red).

Ventuals’ performance has not contributed significantly, accounting for only 0.78% (RoSC). It’s clearly shown that the main revenue of this market is from $HYPE staking yield.

Felix’s fee revenue only accounts for about 4%, reflecting that the profitability of this DEX is still quite challenging.

HyENA’s fee revenue sharing ratio is 8.6%, reflecting an effective deployment strategy.

Notably, TradeXYZ’s total yearly income accounts for 38.7%, indicating that capital stakes are heavily leveraged through volume, and trading fees become the primary source of revenue (36.44%), rather than a secondary one.

Taken together, the estimated revenue and RoSC analysis indicate that:

HIP-3 remains financially attractive for a small set of dominant builders, but capital-inefficient for those unable to capture a significant market share.

3/ Why Is TradeXYZ Dominating The HIP-3 Market?

The first and foremost reason is that XYZ is the first mover on HIP-3 market, which is a superior advantage for this DEX itself. This is also the pioneering DEX allowing equity perps trading on HL, which has never appeared on this platform before. Many traders joining in the crypto world also have engaged in macro and equity trading, but lacked access to equity derivatives in a non-custodial, blockchain-based environment. TradeXYZ has tapped into this unmet need and quickly gain the market share advantage.

The first product on HIP-3 is XYZ100/USDC, which was launched on 13th October, 2025, recorded about $13M in trading volume on that day. Day by day, this figure together with other equity products, continues to surge, helping the XYZ cover the majority of HIP-3 market share (about 90% as the metric below).

Another reason for the current success of this deployer is that XYZ markets currently include equities and commodities quoted in USDC – the most popular stablecoin used as collateral and the quote asset on HL.

On the other hand, Felix and Ventuals also enable equity/commodity and pre-IPO valuations trading pairs but only quoted in USDH. This is a new fiat-backed native stablecoin of HL just launched 3 months ago; therefore, user confidence in this situation is not robust enough to facilitate the trading volume. That’s one of the most plausible reasons why these 2 markets’ performance appear to be inferior to the others’.

In short, TradeXYZ, with the first-mover advantage and a smart choice of the quote asset, leads the HIP-3 market with flying colors. Looking at the current situation, much of HIP-3 market’s success depends on TradeXYZ’s performance, reflecting an imbalance market competition.

SECTION 3: NON-FINANCIAL PERSPECTIVE - WHO IS HIP-3 FOR?

However, if we only look at the mentioned-above financial factors to determine whether a builder should deploy a perp DEX on HL or not, that’s a relatively narrow perspective. Only considering the estimated revenue or RoSC, we can’t firmly decide that Felix, Ventuals or other smaller builders shouldn’t list their perp markets on HL.

From a deployer or a project perspective, in addition to economic view, other factors are also important, even more important than the short or long-term profit.

HIP-3 is a suitable marketplace for the following target builders.

1/ Those With Product-Market Fit But Lacks Of Distribution

Distribution fit refers to a builder’s ability to reach real users with actual trading demand and capital.

For many new builders - already equipped with product-market fit and solid infrastructure (oracles, risk engines, funding logic) - this has become a primary concern.

At launch, Hyperliquid had not yet listed real-world asset (RWA) perps such as equities or commodities. On HyperCore, crypto-native markets like BTC, ETH, SOL, and memecoins already enjoy deep liquidity and mature validator support. As a result, HIP-3 builders have limited competitive advantage when launching additional crypto-native perpetuals.

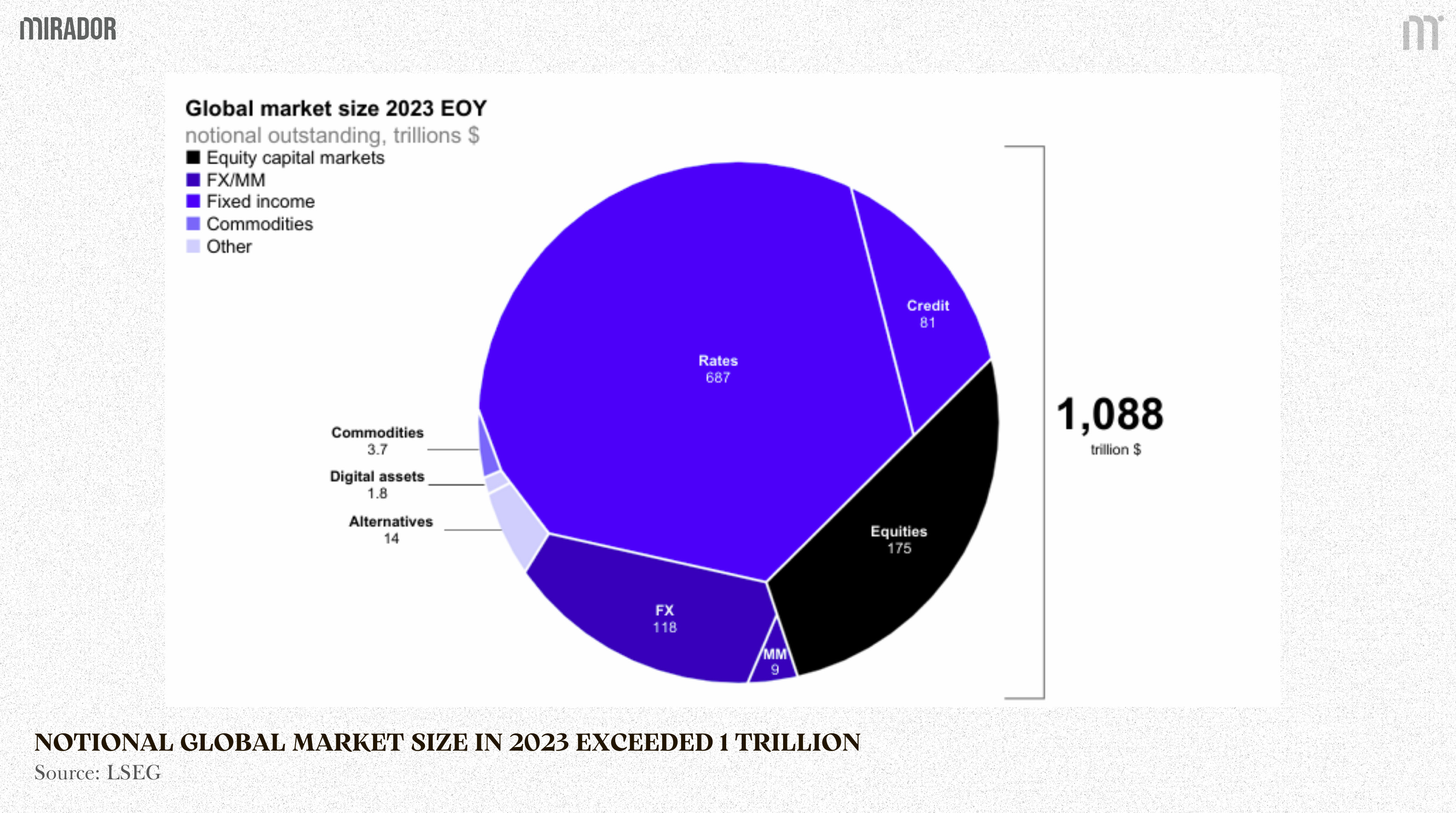

Therefore, a new path is needed to create a differentiation on HIP-3 market. RWAs, with the base of a stably high-quality volume from traditional finance (over $1 trillion) and little volatility (less manipulation risk), appear to be a better option – a product-market fit, especially for TradFi-curious and macro traders.

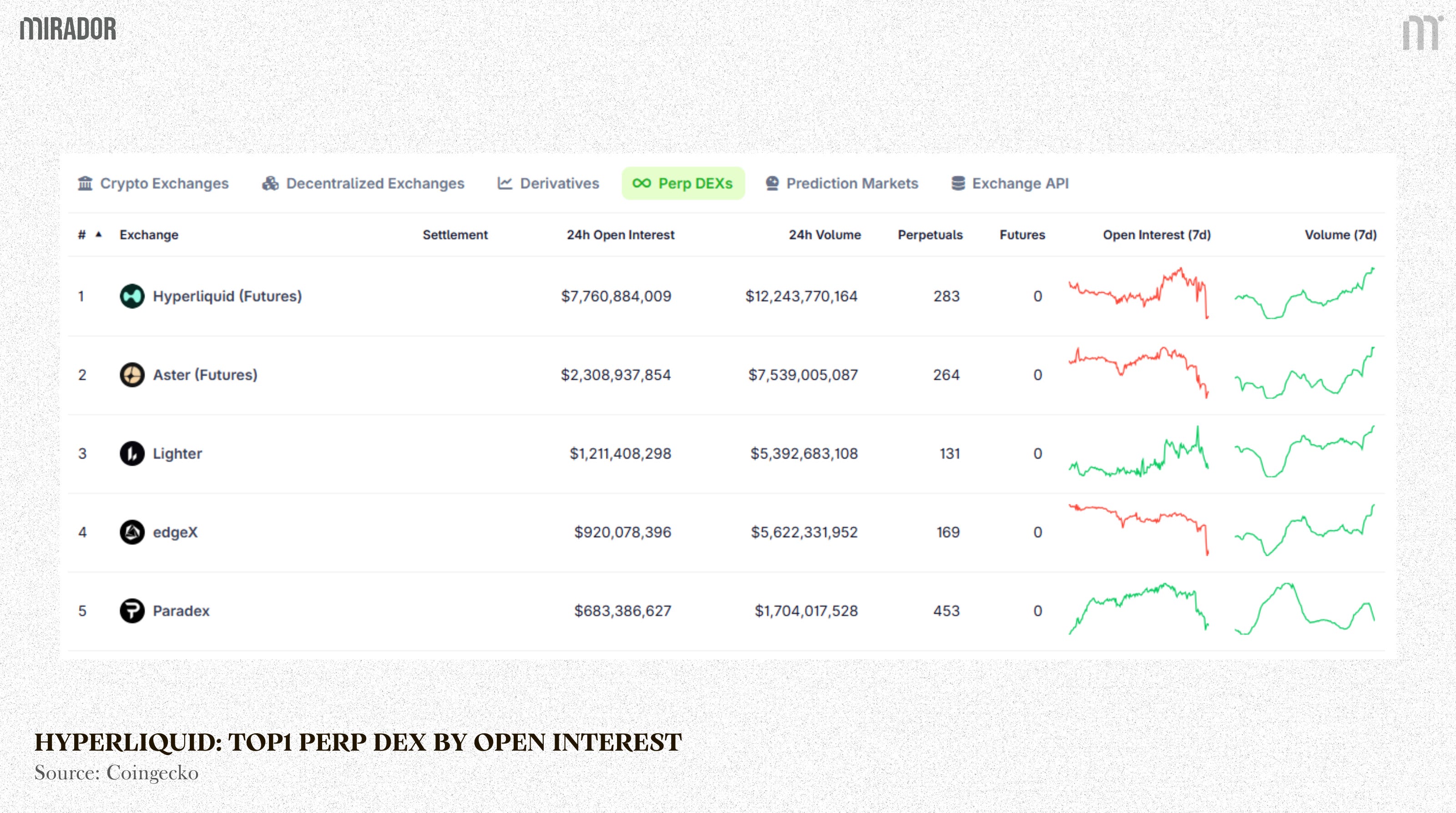

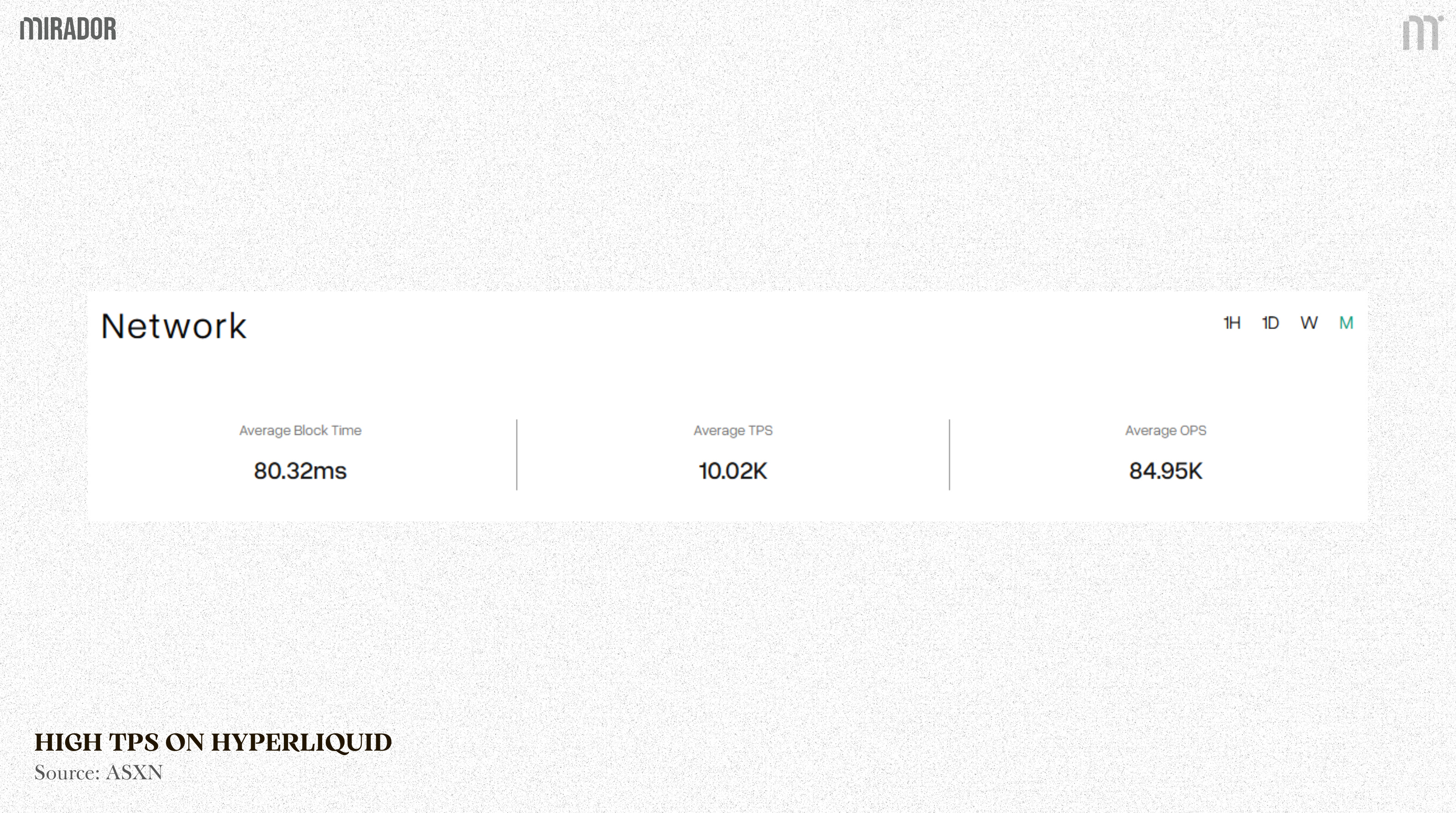

Moreover, HL has many benefits that attract early deployers like XYZ, such as user quantity (nearly 900k), high liquidity and volume (top 1 perp DEX by Open Interest - $7B), a CEX-like UI built on HL Layer-1 blockchain with a smooth trading experience and low latency (currently about 10k TPS).

Considering these factors, HIP-3 is a distribution channel for financial products that fit the market.

2/ Those Who Want To Monetize Their Core Asset

HIP-3 is also a suitable sales channel for a project to list their perp market, in order to amplify the value of the project’s core product.

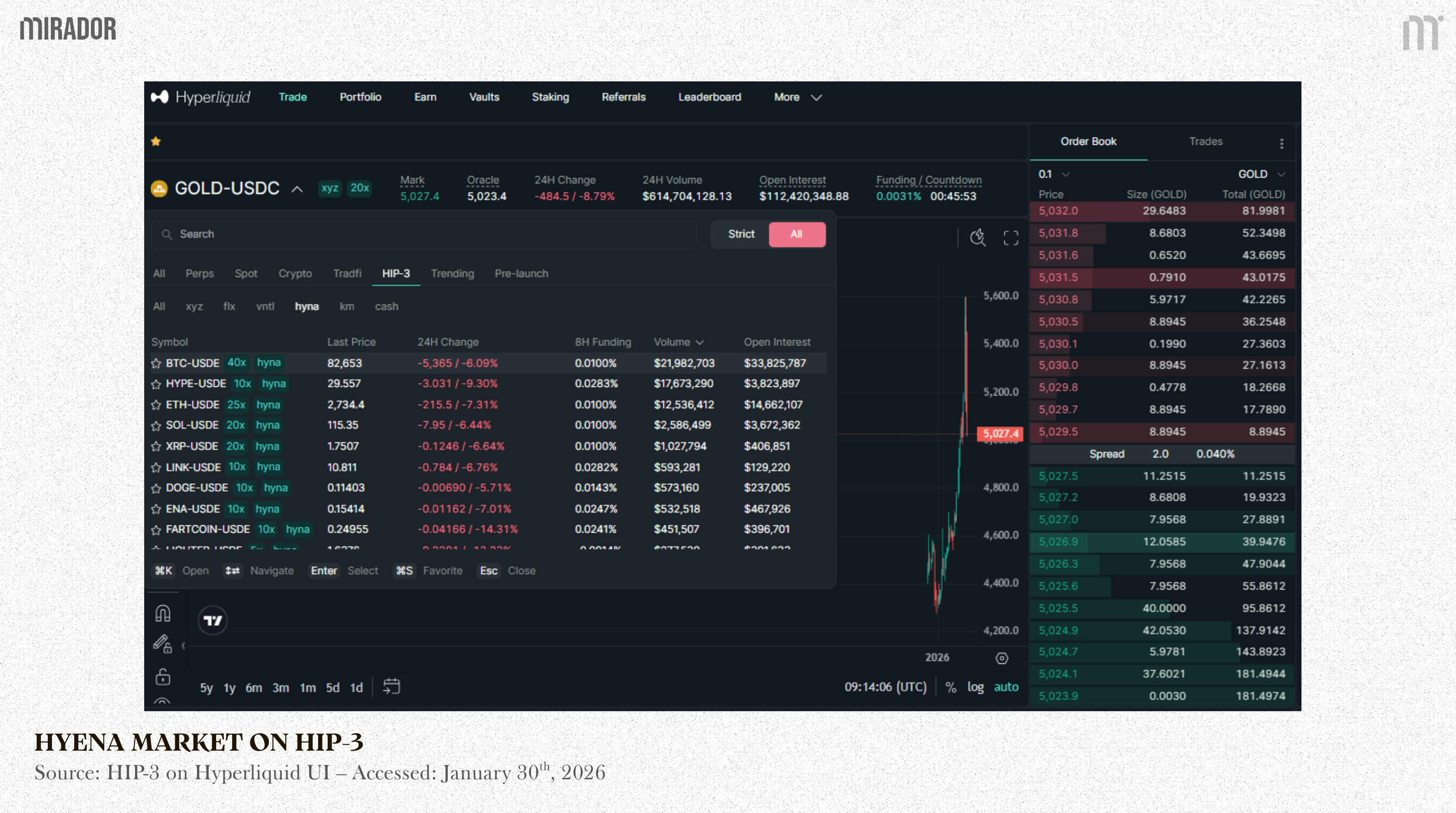

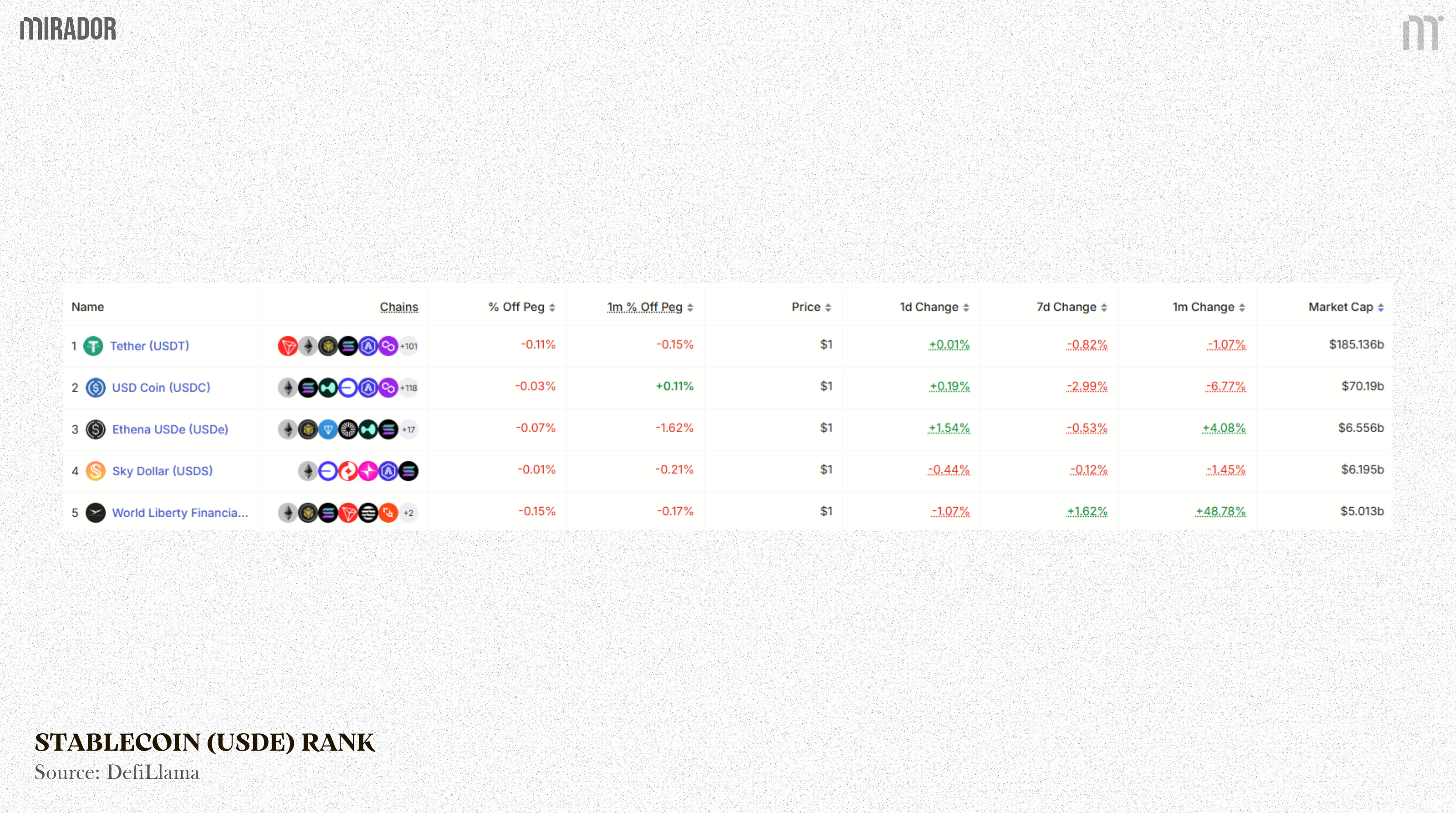

A typical example in this case is Ethena. On 9th December, 2025, HyENA DEX (the collaboration among Based, Ethena and Hyperliquid) went live on HIP-3 perp market. Most trading products on this market are crypto-native perps, but quoted in USDe – a stablecoin of Ethena launched in the early 2024, such as BTC/USDE, ETH/USDE.

The main purpose of Ethena listing a perp market on HIP-3 is not just to earn trading fee, but creating indirect demand for their core asset, USDe.

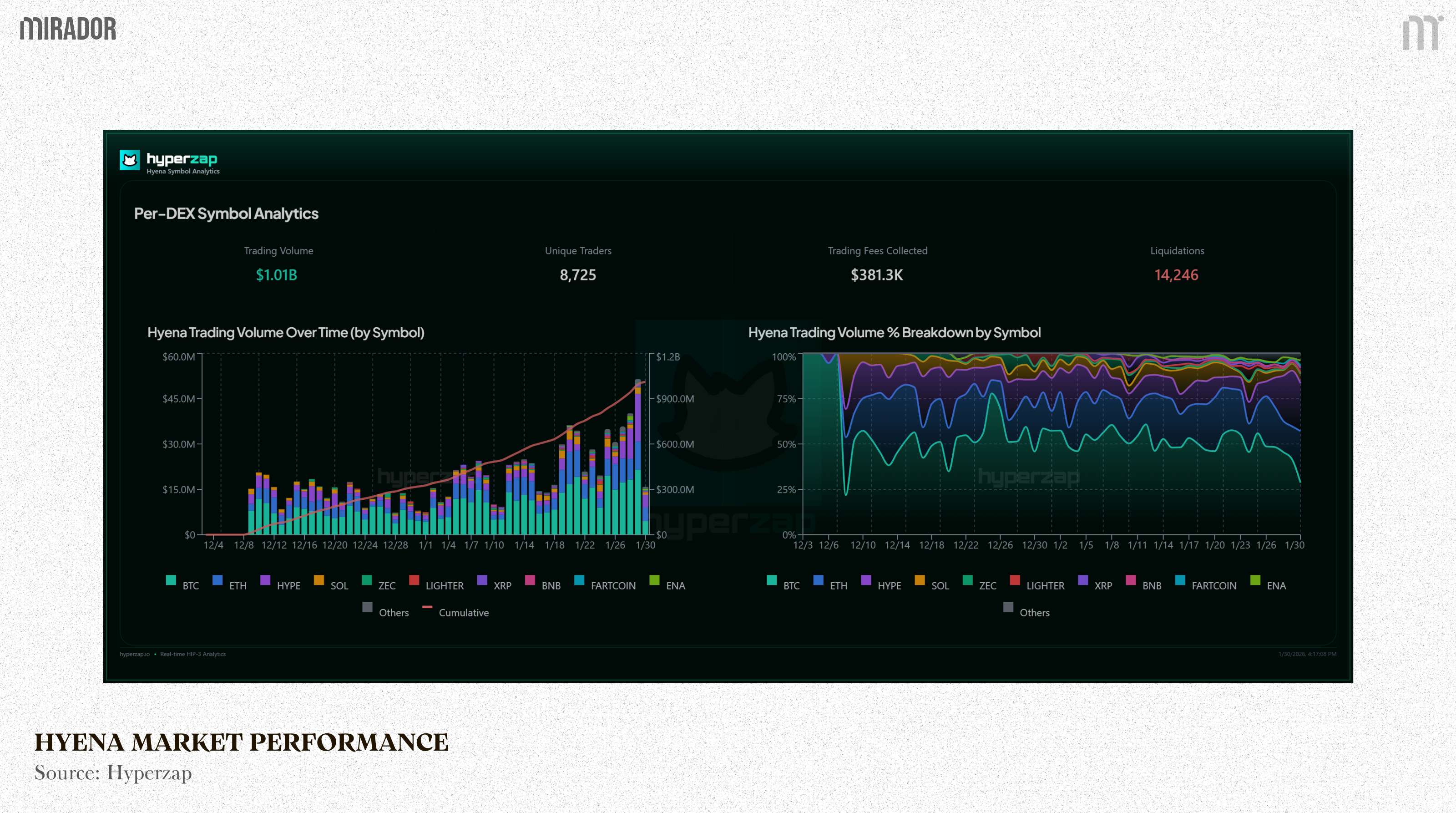

Within over 50 days of launch, the HyENA market recorded over $1B in trading volume and generated more than $380k in trading fees. With volumes continuing to trend upward, HyENA is beginning to close the gap with established HIP-3 deployments like TradeXYZ.

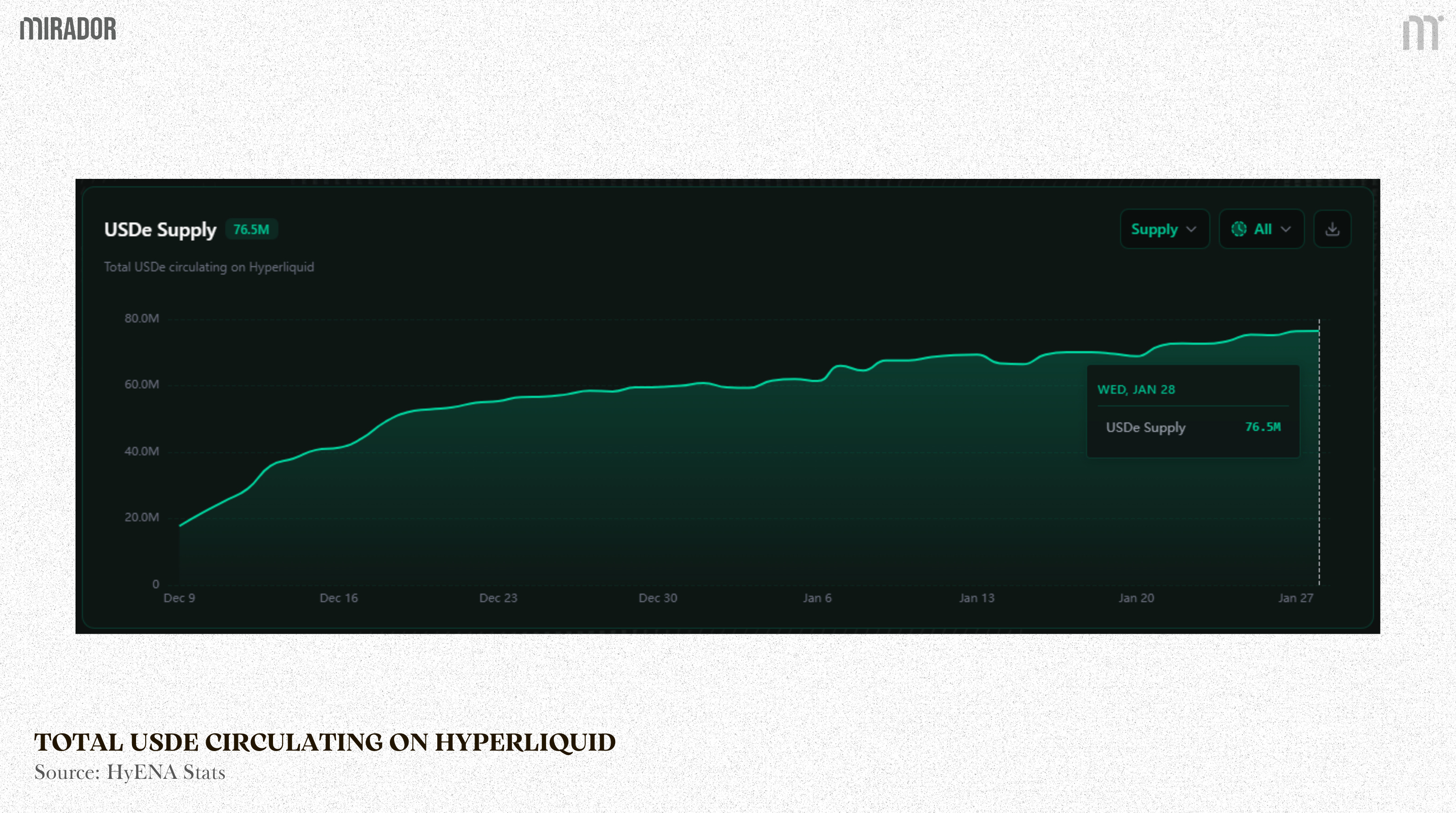

The more trading volume this market gets on HIP-3, the higher USDe exposure and usage will be. The metric below reflects the increase in the USDe supply since the launch of HyENA. Currently, over $75M USDe has been used on Hyperliquid and this number is still growing, showing the potential of a USDe-based margin trading market.

3/ Those Who Want To Seize The First-Mover Advantage And Trust In Hyperliquid

HIP-3 is a fit to the builders with a strategic vision, especially those who can grasp the opportunity of being first on the battlefield.

Take Felix and Ventuals as an example. Even though the trading performance of these two markets remains modest, only about 0.3-2% HIP-3 market share, what they are betting is the future of their products. Both protocols focus exclusively on RWA-linked products (stock indices like TSLA, MAG7, OPENAI...) but quoted in USDH.

While USDH, Hyperliquid’s native fiat-backed stablecoin, is still early-stage and has yet to be fully stress-tested, its future adoption could materially reshape this segment of the ecosystem. Like Ethena and its stablecoin, which was launched two years ago, now has become one of the largest stablecoin in the crypto world.

USDH is just 3 months old, and still has a long journey ahead, together with HL ecosystem. If USDH usage increases further in the future and RWA trends improve, Felix and Ventuals will benefit even more as early movers, and vice versa.

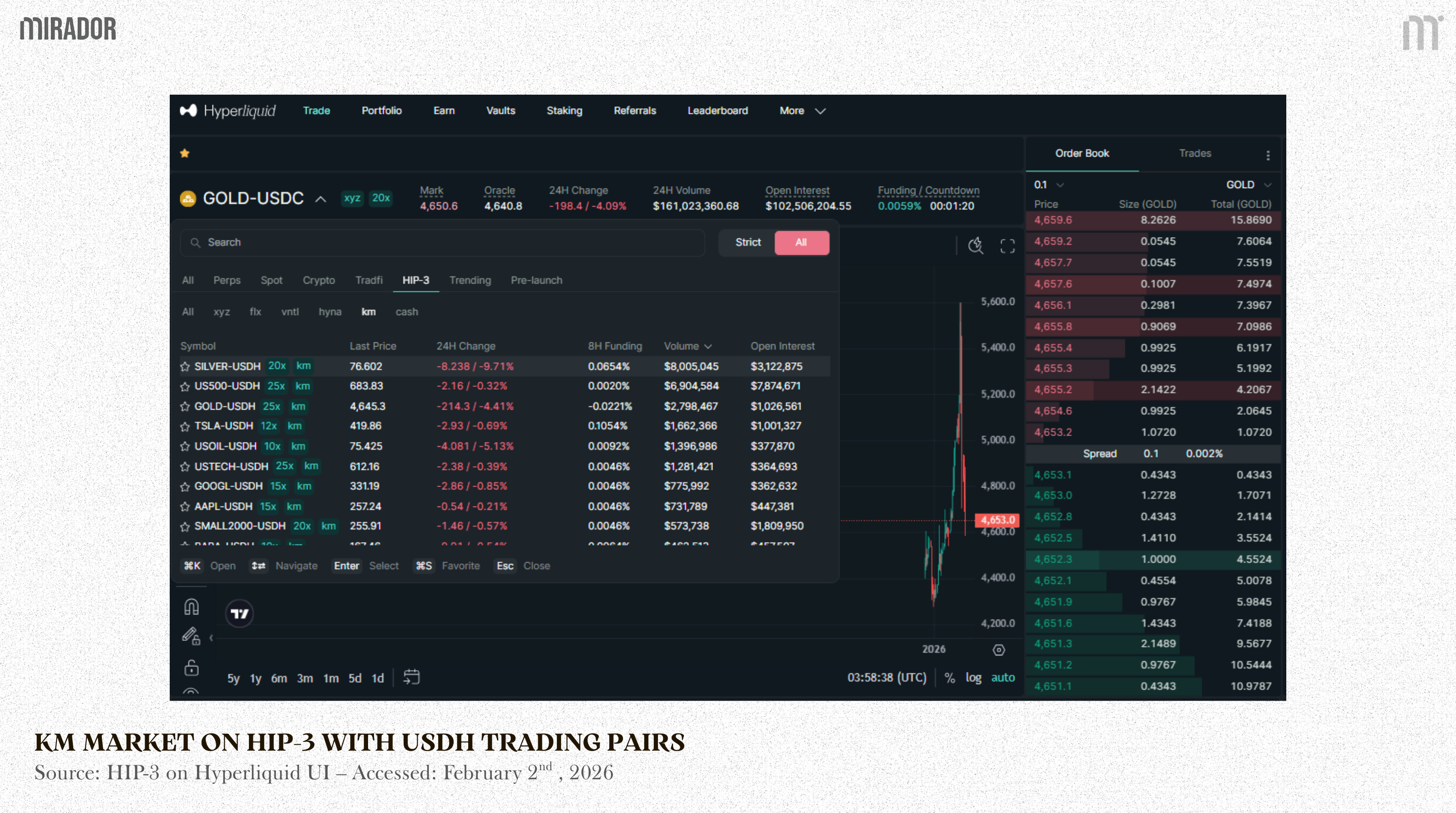

Notably, competition in USDH-denominated markets is already intensifying, specifically with the entry of KM (markets by Kinetiq). KM has processed transactions totaling $680M in just over 3 weeks, underscoring the latent demand in this market.

Anyway, this will be a long-term journey that only large builders can survive.

SECTION 4: LOOKING AHEAD - WHAT CAN LATE ENTRANTS DO ON HIP-3?

TradeXYZ is a pioneer in RWAs perp trading, Felix and Ventuals are pioneers in RWAs trading products quoted in HL’s native stablecoin, and Ethena (HyENA) is pioneer in monetizing their core asset – USDe.

So, a strategic question is: What can late entrants do on HIP-3?

HIP-3 is not completely closed. It’s only closed to small builders with short-term vision, but not the opposite side.

Large builders can also choose the same path as Ethena (HyENA) to route the volume and exposure to their core assets. Currently, most of trading pairs on HL are quoted in USDC, USDH and USDe; and builders can choose to list HIP-3 perp products quoted in other top stablecoins. For example, Sky can deploy a DEX to boost their DAI/USDS stablecoin exposure.

Besides, product-market fit is always an essential factor to consider before deciding whether to list a perp market on HIP-3. HIP-3 needs novel markets that meet the trader demand.

One of the promising primitives that remains unexplored on HIP-3 is prediction market–based perps. At present, RWAs dominate HIP-3 deployments but there’s still no prediction market perps listed to track probabilistic or event-driven outcomes. This market is highly potential because of its high trading volume.

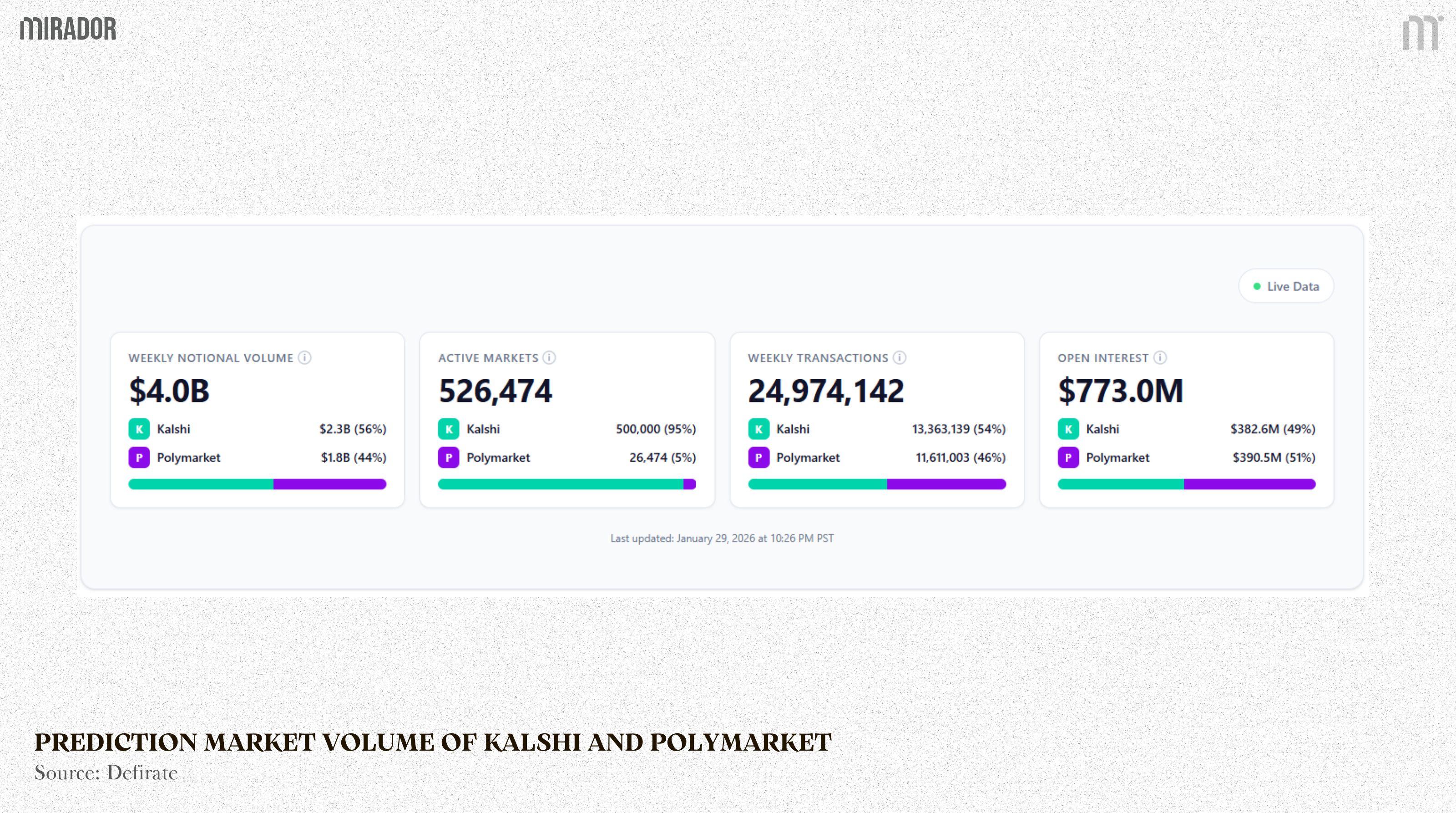

As can be seen in the figure below, every week Polymarket and Kalshi – the leading prediction markets today - attract over $2B in notional volume. This figure shows that the demand for speculation and hedging based on events is very high.

Also, as predicted by 21shares, by 2026, prediction markets, like Polymarket and Kalshi, are expected to surpass $100B in annual trading volume, onboarding millions of users as real-world events in geopolitics, sports and beyond are monitored, traded and registered onchain.

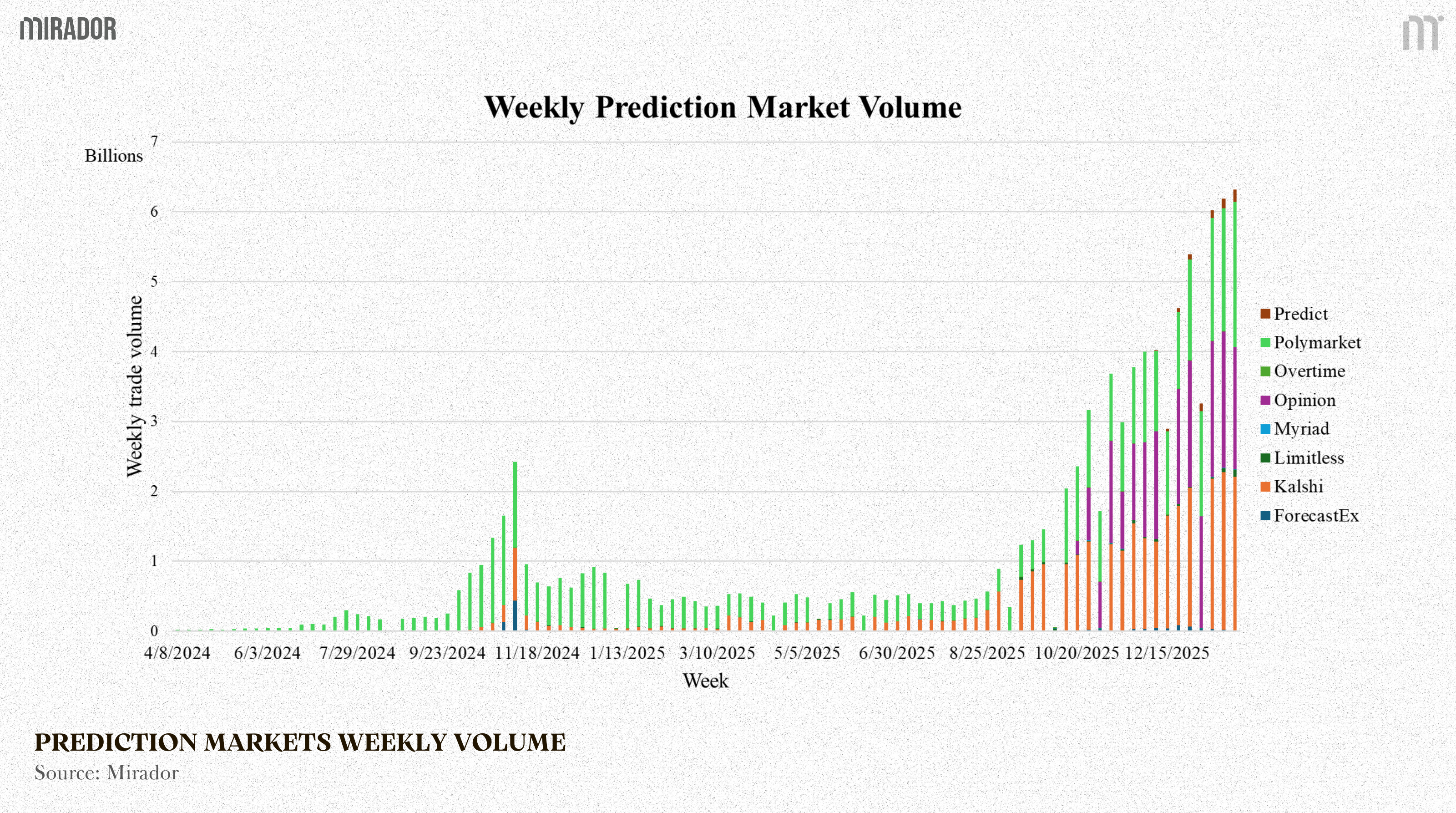

If we look at the weekly volume of this market, the total volume has just exceeded $6B, reflecting a high trading demand.

With HIP-3’s permissionless model, deployers can try transforming “event-based” prediction markets into 24/7 leveraged perp markets. This could be a suitable direction for late entrants as they don’t need to compete directly with equity markets, but can instead focus on product innovation.

In fact, with the recent introduction of HIP-4, which aims to build upon HIP-3 by enabling outcome and prediction contract primitives, if builders are afraid of being a HIP-3’s late entrant, becoming an early mover on HIP-4 with prediction market is also worth considering.

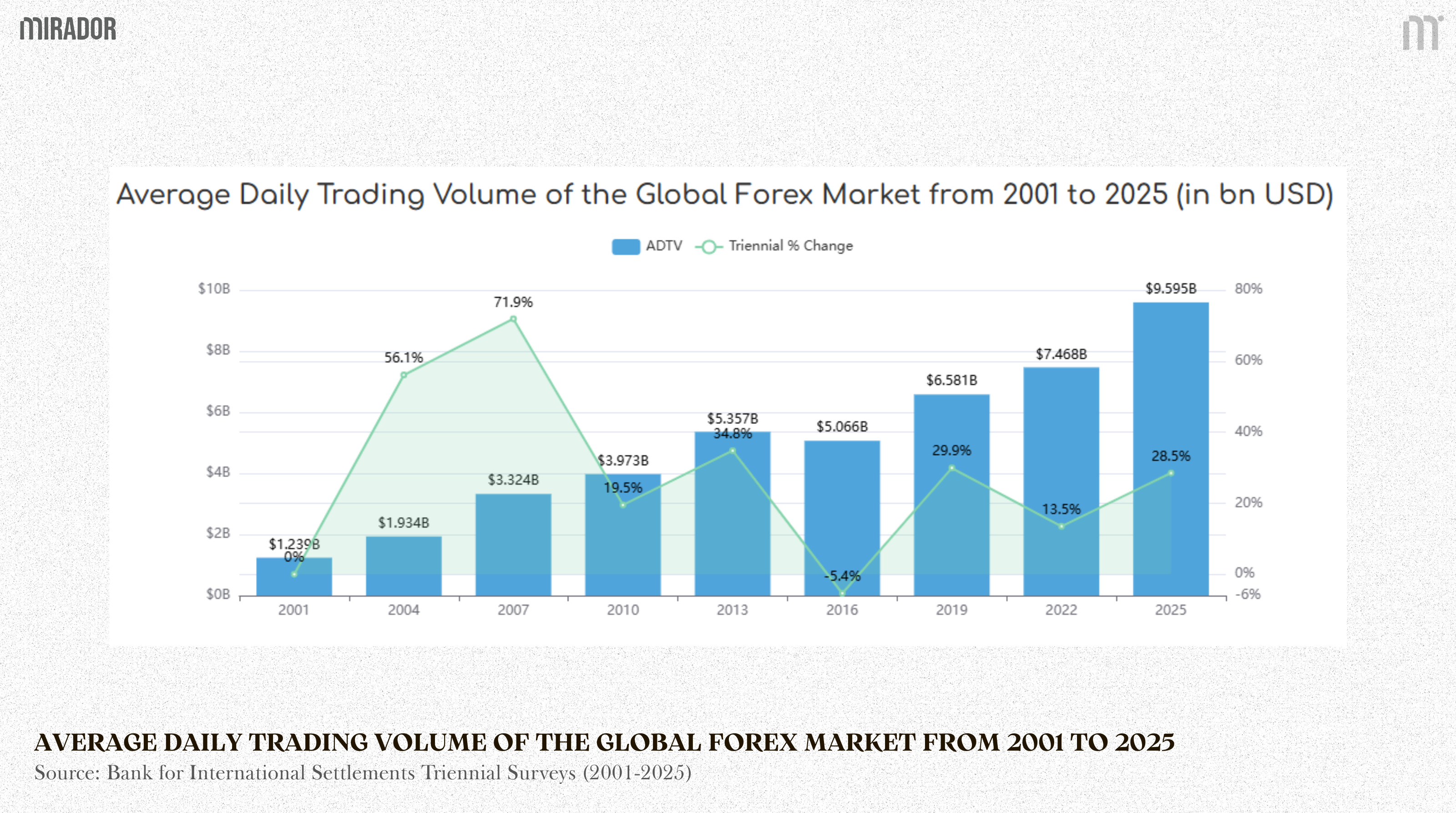

Besides, large segments of traditional derivatives markets remain largely untapped in crypto-native perp venues. Looking at the daily trading volume of the global forex market (nearly $10B), but perp products linked to FX are still very rare on on-chain platforms. So, listing a perp DEX like this on HIP-3 can also be a potential path.

Hyperliquid in general, and HIP-3 in particular, requires niche and differentiated markets to drive expansion. And from the project’s perspective, this product aligns well with current trading demand.

CONCLUSION

To sum up, HIP-3 is not a money printer for every builder but only for those with great resilience and capital to survive a long-term journey.

To remain competitive under current conditions, builders must not only meet Hyperliquid’s listing requirements but also deliver products that align with prevailing market narratives.

For some participants like Ethena, HIP-3 functions less as a profit center and more as strategic infrastructure.

And for those who place long-term trust in the growth of Hyperliquid, HIP-3 is still an open gateway for them to expand in the future.

DISCLAIMER

This article is an independent research-based analysis of the HIP-3 framework and its incentive structure for builders on Hyperliquid. It aims to evaluate HIP-3 from an economic and strategic perspective, rather than to promote any specific deployment or project. From there, we hope readers can form their own perspective on the associated opportunities and risks.

All views presented are based on publicly available information and reflect the state of the market at the time of writing. Outcomes for individual builders may vary significantly depending on execution, capital strength, risk management, and broader market cycles. This content is for research and educational purposes only and should not be interpreted as financial or investment advice.