HYENA: THE PERP DEX BUILT AROUND PRODUCTIVE MARGIN

A case study of USDe margin and capital-efficient perps under HIP-3

INTRODUCTION

HIP-3 is transforming Hyperliquid from a single perps DEX into a permissionless derivatives marketplace. Among the first HIP-3 deployments, HyENA stands out as a perps DEX built on Hyperliquid with USDe margin, backed by the strategic collaboration between Ethena, Hyperliquid and Based.

Despite going live for just over one month, HyENA has already attracted notable attention due to its rapid growth and unique margin design.

This article provides a detailed breakdown of HyENA’s economic design and trading mechanics, and evaluates whether it offers a compelling value proposition for traders.

KEY TAKEAWAYS

In this article, we explore the inner workings of HyENA perps DEX and examine its potential under the trader’s perspective through the following main sections:

Section 1: Explore the operating model of HyENA

Section 2: Explore the benefits that users and protocols parties will gain

Section 3: Examine the potential of trading on HyENA from the user’s perspective

SECTION 1: HYENA OPERATING MODEL

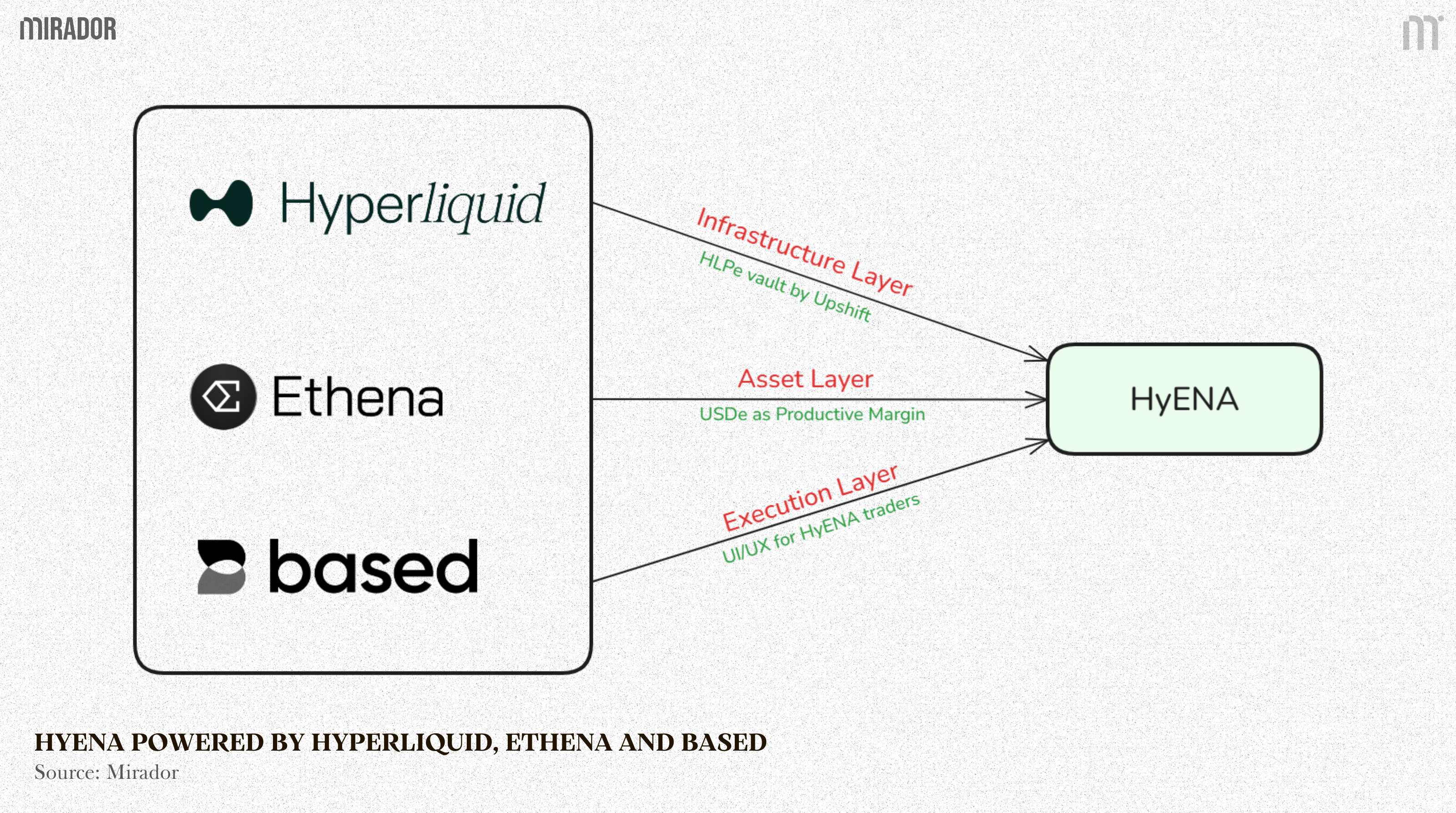

HyENA is a perp DEX deployed on HIP-3 (Builder-Depl oyed Perpetuals Improvement Proposal of Hyperliquid) standard, with the combination of 3 main layers powered by 3 following protocols: Hyperliquid, Ethena and Based.

1) Hyperliquid HIP-3 – Infrastructure Layer

Before HIP-3, only the core team can list perpetual markets on Hyperliquid. In order to solve this limitation, HIP-3 was introduced as a framework born to allow any builders to deploy their perps DEX permissionlessly, as long as they meet certain listing requirements.

One of the most notable requirement is related to staking amount, which is currently 500k $HYPE, worth roughly $15M. It means HyENA was launched only after Ethena successfully staked the required 500k $HYPE, serving as a safeguard against malicious or low-quality deployments.

Hyperliquid permits HyENA to be deployed as a separate perp DEX while inheriting the Hyperliquid’s core infrastructure, including orderbook, matching engine, and low latency of this protocol. Moreover, HIP-3 allows every deployer to customize their own market, collateral, fees, and incentives.

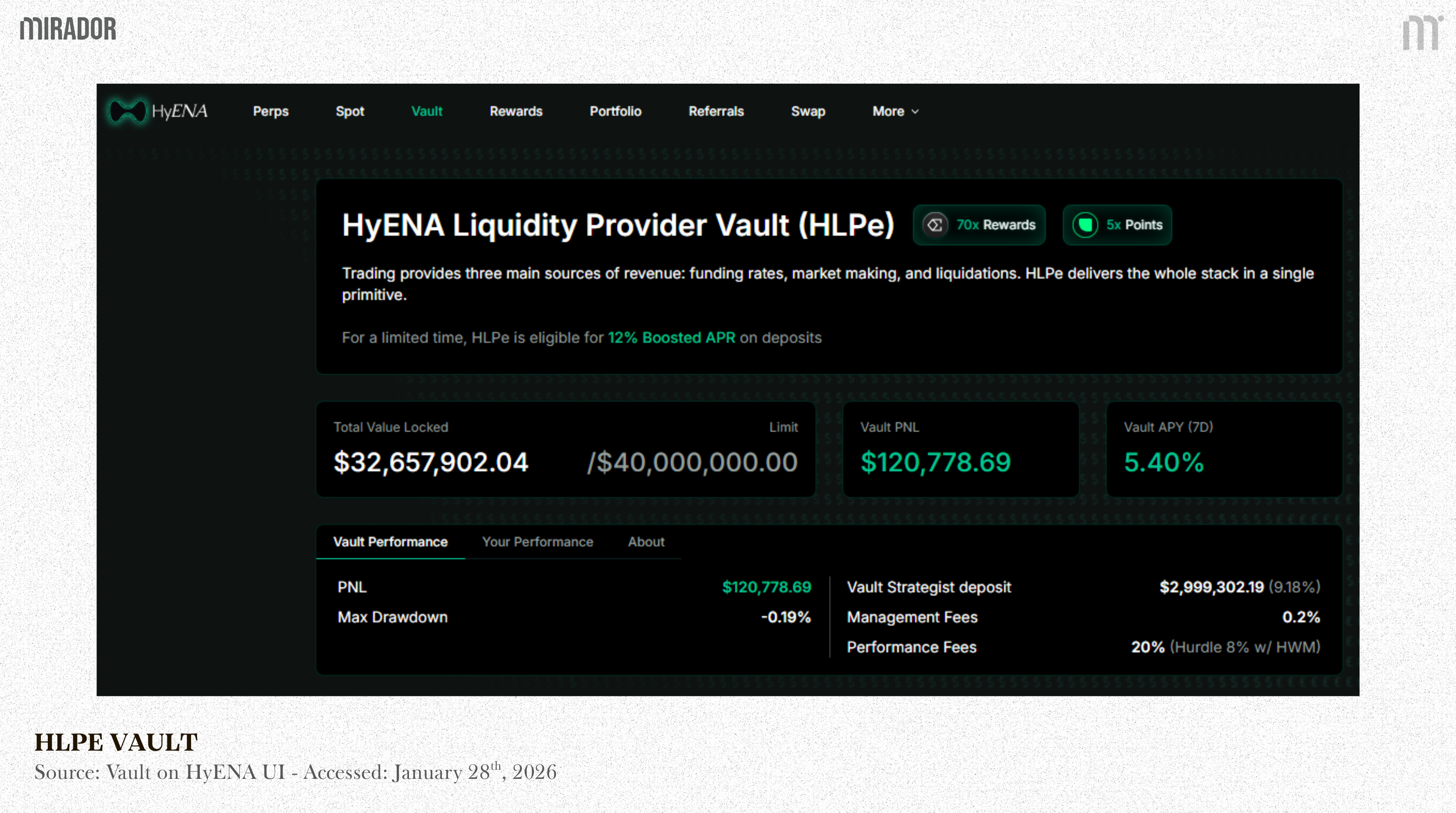

Thanks to HIP-3, HyENA users enjoy the same trading experience as on the Hyperliquid DEX. Hyperliquid has HLP vault acting as the protocol’s liquidity layer through multiple market making strategies, performing liquidations, and accruing platform fees. Likewise, HyENA also has HLPe vault (managed by Upshift), which fulfills an equivalent role, but the only difference is that HLPe vault is used for market making strategy, it is not directly involved in liquidations or Auto-Deleveraging (ADL).

From a structural perspective, HyENA can be viewed as a “mini Hyperliquid DEX”, inheriting the same execution and liquidity architecture while operating as an independent HIP-3 deployment.

2) Ethena – Asset Layer

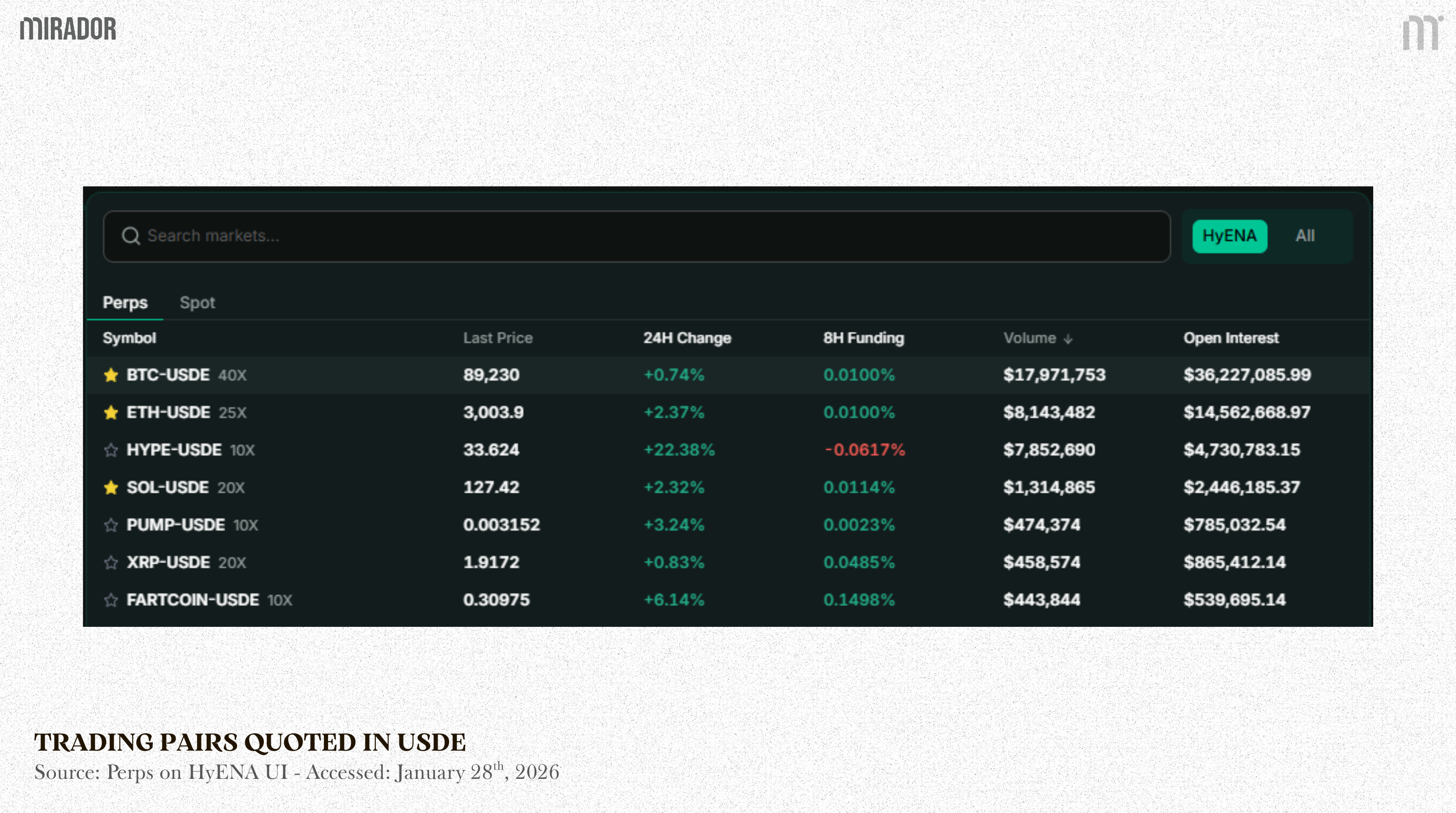

Most trading products on HyENA are native tokens quoted in USDe, like BTC/USDe, ETH/USDe. So traders are required to deposit USDe as maintenance margin when opening a position on this DEX.

In return, traders can earn a certain extra USDe reward (APR) on their full spot and perps margin balance powered by Ethena. Currently, the base yield rate applied to traders with available USDe is 4.5%/year. It means that in addition to the trading PnL, traders can earn an extra 4.5% APR, which will be applicable to all idle balances and balances used to margin positions.

With this incentive, margin yield can partially offset trading costs such as fees and funding, depending on position direction and funding conditions.

How can USDe keep its peg and earn yield for stakers?

USDe (Ethena USD) is a yield-bearing synthetic dollar launched in February 2024, not backed 1:1 by cash or short-term US Treasury bills like USDC but via holding liquid stables like USDC and USDT and the delta-neutral hedging mechanism, where Ethena:

Long spot ETH (or LSD ETH)

Short perpetual ETH with equivalent volume

For every dollar of USDe, Ethena will hold an equivalent amount of crypto as collateral while going short on CEXs like Binance. Or:

1 USDe = $1 of ETH + Short 1 ETH / USD Perpetual

By this way, Ethena neutralizes ETH price volatility, creates a value of approximately 1 USD for its stablecoin.

Moreover, because perpetual markets typically have a positive funding rate, Ethena collects funding fees plus the basis spread from that short position. This is the main source of revenue to pay for USDe stakers, who will receive sUSDe (Staked USDe) after staking as a receipt to gain yield afterwards.

3) Based – Execution Layer

The final party in the development of HyENA DEX is the Based team, which is also the leading Hyperliquid application in revenue. Based acts as an execution layer, which provides front-end trading and enhances UI/UX for HyENA traders.

SECTION 2: TRADERS AND PROTOCOLS PERSPECTIVE - WHAT WILL THEY BENEFIT?

1) What Will Traders Benefit?

The biggest difference between HyENA’s users and Hyperliquid’s or non-HyENA’s native users is the lazy yield generated from USDe margin.

At its core, USDe doesn’t generate any yield from the stablecoin itself. On Ethena, sustainable yield is earned only when USDe is staked into sUSDe, with returns primarily sourced from protocol revenue such as funding and basis trades. So theoretically, if you only hold USDe without locking or staking it, you won’t earn any yield.

Besides, on HyENA, USDe holders are not required to stake USDe to earn yield. Instead, USDe used as margin becomes effectively immobilized within the trading system, creating a form of sticky supply. And this reward is also derived from Ethena’s revenue. Ethena designs yield as an incentive layer for traders with USDe margin, aligned with Ethena’s objective of securing circulating supply while encouraging USDe adoption in derivatives trading.

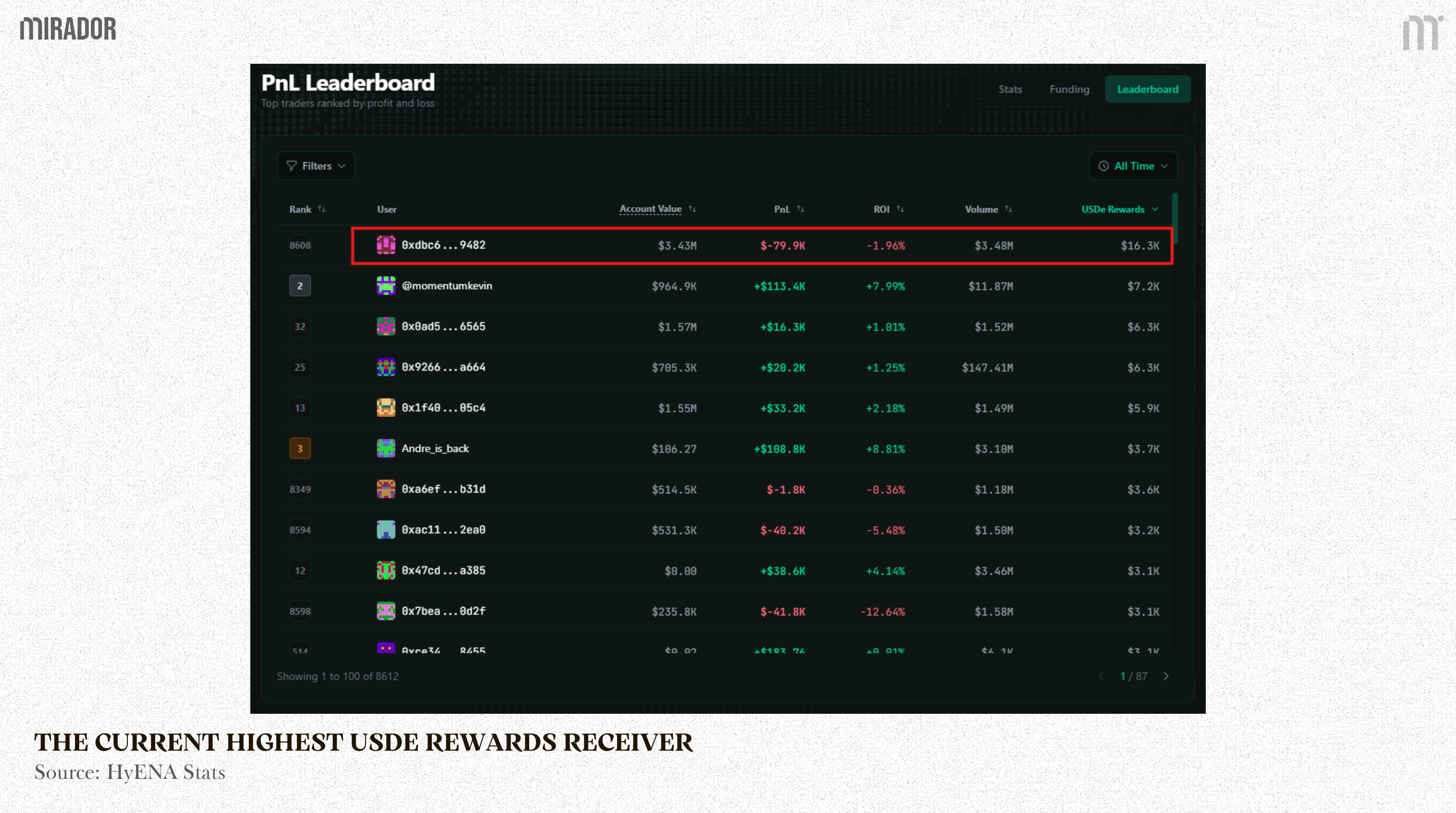

After one month of launch, HyENA has allocated over $400k to the eligible USDe holders. Currently with nearly 9k users, on average, each user is qualified for receiving $45. This is just a hypothetical averaging calculation since in practice, USDe rewards are highly proportional to traders’ volume.

Some traders may earn a relatively huge amount of incentives, like in the picture above, the highest USDe reward ($16.3k) currently belongs to a whale’s wallet address ***9482 with the total spot and perp balance of over $3M (by Flowscan) while other smaller fishes are earning less. As rewards are distributed on a daily cadence to user’s HyperCore balances, based on rolling average user balances, this amount can grow more.

About the rolling average user balances, it can be understood by the way that the system takes multiple balance points over time and calculates the average to determine the “bonus balance” for that day, instead of looking at the balance at just one point in time.

Example:

If you hold USDe inconsistently throughout the day, assume your balance record looks like this:

00:00 - 0 USDe

06:00 - 1,000 USDe

12:00 - 1,000 USDe

18:00 - 0 USDe

Then, the average balance = (0 + 1000 + 1000 + 0) / 4 = 500 USDe

At the current 4.5% base APR, your USDe reward would be 22.5$/year

Even if you have 1,000 USDe at one point, the bonus will be “almost the same” as if you held an average of ~500.

However, if your balance stays at 1,000 USDe every day, the average would be 1,000 USDe

And with 4.5% APR, your USDe reward would be 45$/year

NOTE: The HyENA’s documentation only mentions “rolling average user balances” but doesn’t specify the timeframe or formula, so this is just a hypothetical example for readers to understand the basic mechanism behind reward calculation.

So, what traders benefit from HyENA is the bonus that can be passively earned from the USDe margin, and how much it is depends on their perps and spot balance.

2) What Will Ethena Benefit?

Aside from the collected trading fee, thanks to the launch of HyENA and its positive performance, the USDe adoption and supply has increased.

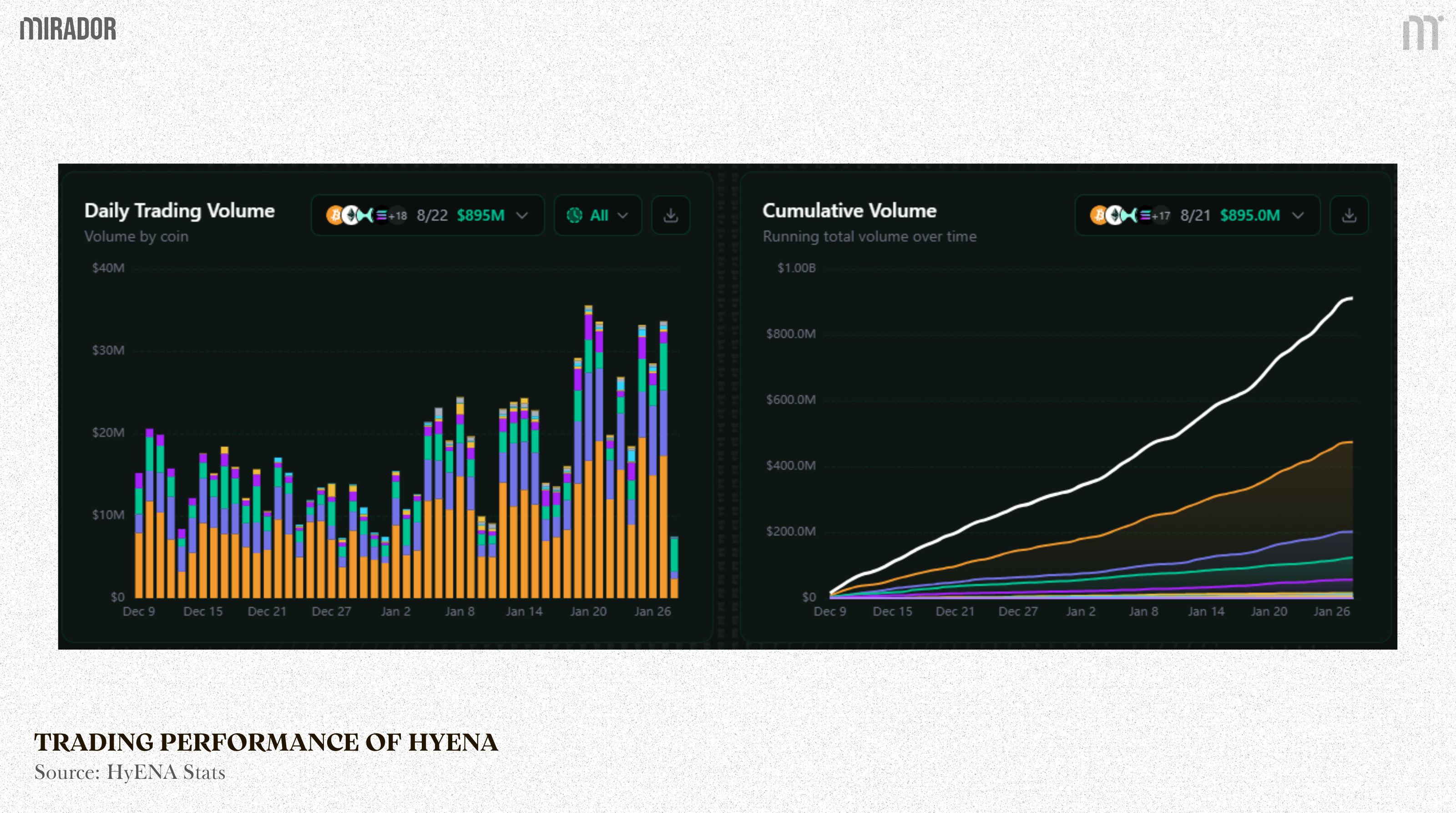

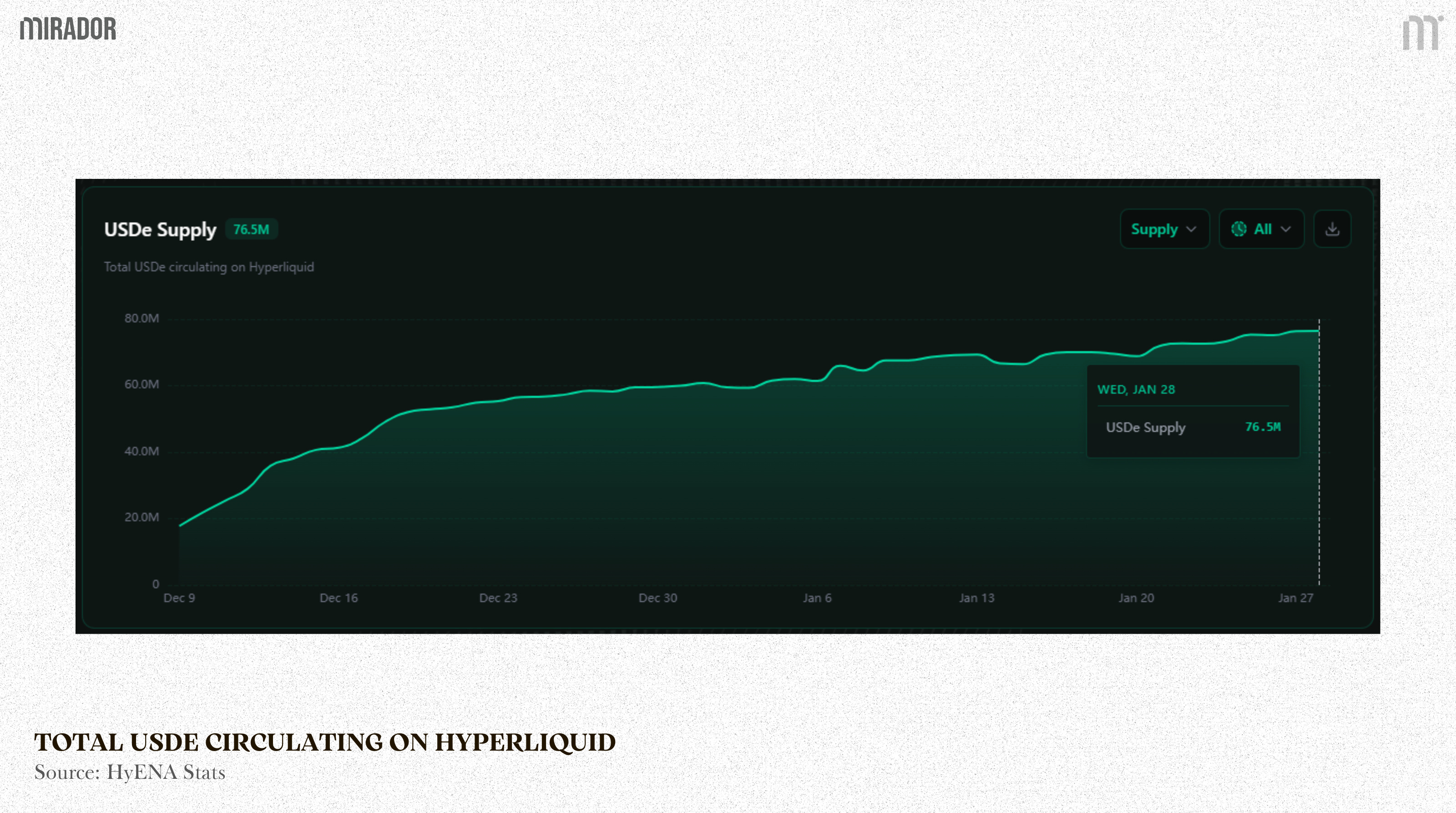

Currently, the total trading volume gained on HyENA HIP-3 market is over $900M, resulting in the USDe supply increase on Hyperliquid, nearly $80M in over 1 month and counting.

If the quantity of USDe margin is getting higher, it creates a sticky demand for USDe. As mentioned above, when traders use USDe as collateral, this amount will be locked in the trading system. ~$80M USDe on Hyperliquid means that it’s not available for sale on the CEX, not sitting idle in the wallet, and not easily withdrawn if HyENA traders still keeps their positions.

As a result, from a strategic view, this not only improves Ethena’s hedging efficiency at scale, but also accelerates USDe’s transition from a passive stablecoin into a productive on-chain collateral asset. And as long as USDe continues to be used as collateral on Hyperliquid or HyENA, the risk of mass redemption will be reduced.

Moreover, Ethena is gaining distribution without needing to build a DEX from scratch. HIP-3 in general, and HyENA specifically, inherits the high performance margining and order book system of Hyperliquid. As such, Ethena can gain access to deep trader liquidity without bearing the cost and complexity of building its own derivatives infrastructure.

3) What Will Hyperliquid Benefit?

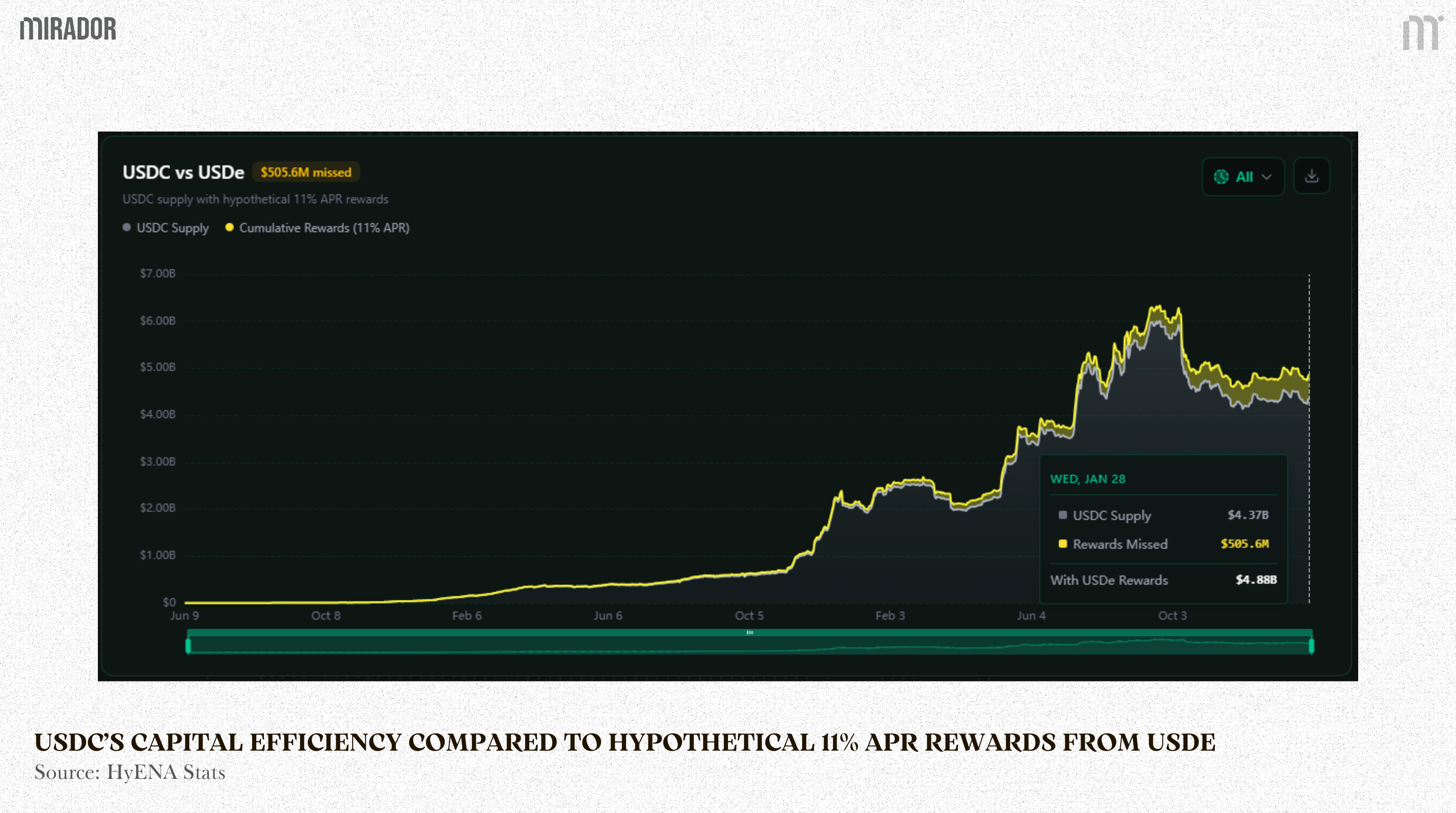

Not to mention the collected trading fee, one of the biggest issues that Hyperliquid can solve is the capital inefficiency in the idle USDC locked as collateral. Most of financial products on Hyperliquid are trading pairs quoted in USDC, whose total supply on this protocol is around $4B. However, as only used as the maintenance margin without bearing any lazy yield, this huge amount is considered inefficient in usage.

With USDe on HyENA as yield-bearing margin, with the current base APR around 4.5%, not to mention the boosted reward at the first initial month (over 7%), this can be an effective solution for Hyperliquid to handle the capital inefficiency.

As seen in the hypothetical metric above, if USDC margin also goes with 11% APR rewards as the model of USDe, the all-time reward would be over $500M. And even only with the base APR (4.5%), the reward would be around $196M – the amount that should have gone to the USDC holders’ wallet but was missed out on.

In short, between Ethena (with higher USDe exposure) and Hyperliquid (with enhanced capital inefficiency), HyENA is a product of a win-win relationship.

SECTION 3: IS HYENA A PROMISING INVESTMENT CHANNEL FOR TRADERS? WHICH POTENTIAL RISKS SHOULD A TRADER BE AWARE OF?

To answer the question: Is HyENA a promising investment channel for traders?

We are to examine the profitability of trading on HyENA HIP-3 from a trader’s perspective.

1) Profitability

Obviously, profit is what traders care most when it comes to trading.

Not to mention the trading PnL (as this depends on the profit-making potential of each individual), is HyENA financially attractive enough for traders to join the game?

At present, according to HyENA team, USDe reward is configured at the base 4.5% APR, the same as sUSDe staking rate on Ethena. Specifically:

Holding USDe as spot on HyENA earns a ~4% APR.

Opening a short position on USDe-margined perpetual pairs on Based/HyENA earns a ~4% APR on margin.

Opening a qualifying long position on USDe-margined perpetual pairs on Based/HyENA earns a ~12% APR on margin (this is boosted reward during HyENA’s initial month only).

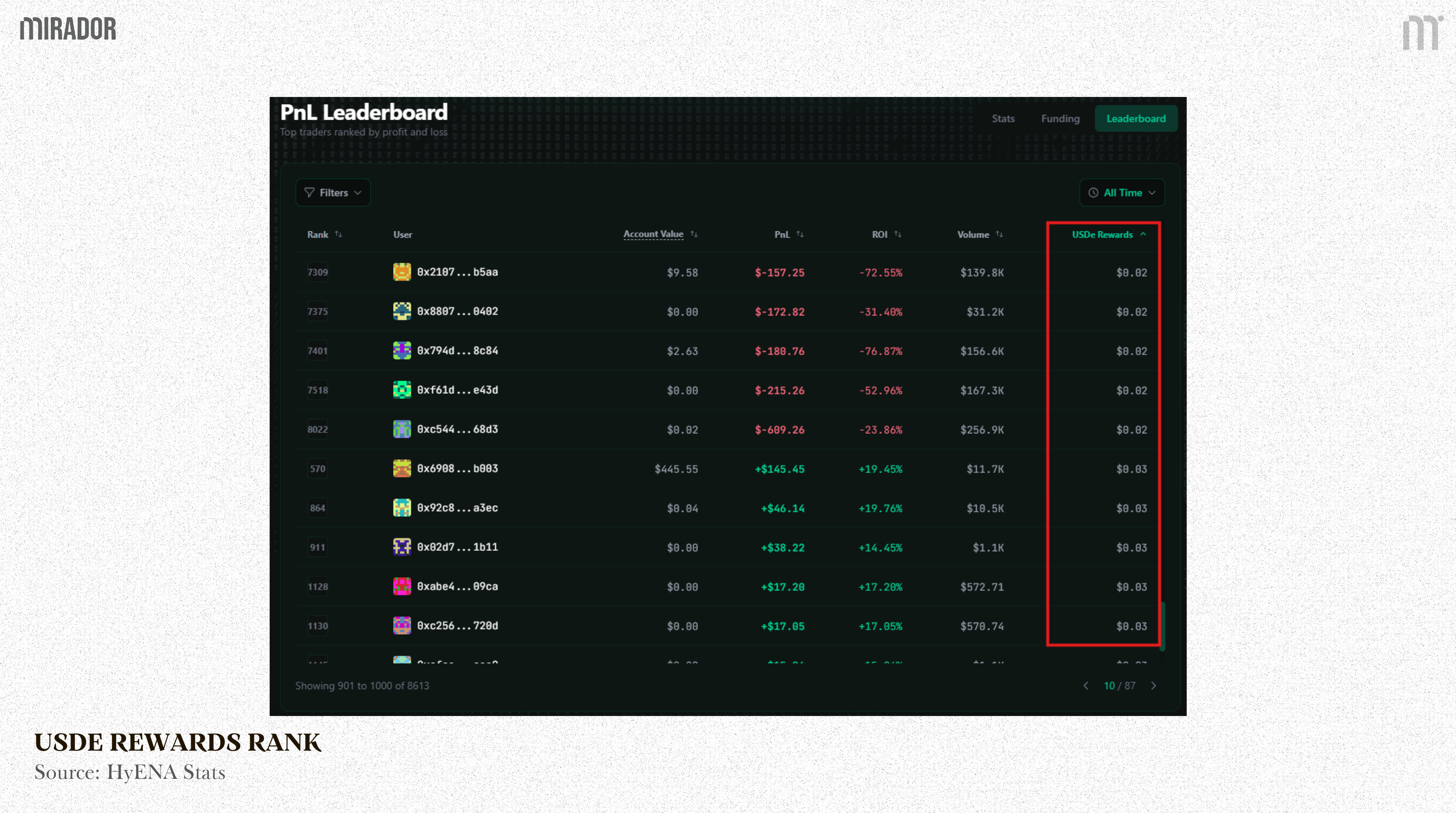

USDe reward is a great bonus for USDe holders on HyENA, but more attractive for large holders. All HyENA’s users automatically earn native USDe rewards on their full spot and perps margin balance powered by Ethena. The more your spot/perp balance, the higher reward you will receive. This also means that rewards are inherently size-biased, favoring large balance traders and institutions over smaller retail users.

As the metrics above, many traders with small spot/perps balance only collect a small amount of USDe rewards. In the unfavorable cases where the trading PnL is negative, USDe can’t compensate for the traders’ losses.

USDe reward is basically an incentive for users to trade on HyENA which increases USDe’s exposure for Ethena protocol. If large holders or traders in general know how to take advantage of this mechanism, they can benefit more than others.

2) Other Potential Concerns

Beyond the reward, as a trader, you should also be aware of other potential issues that might arise during the trading process. The two main concerns to take into account is the depegging risk of USDe and the oracle risk of HyENA.

Depegging Risk

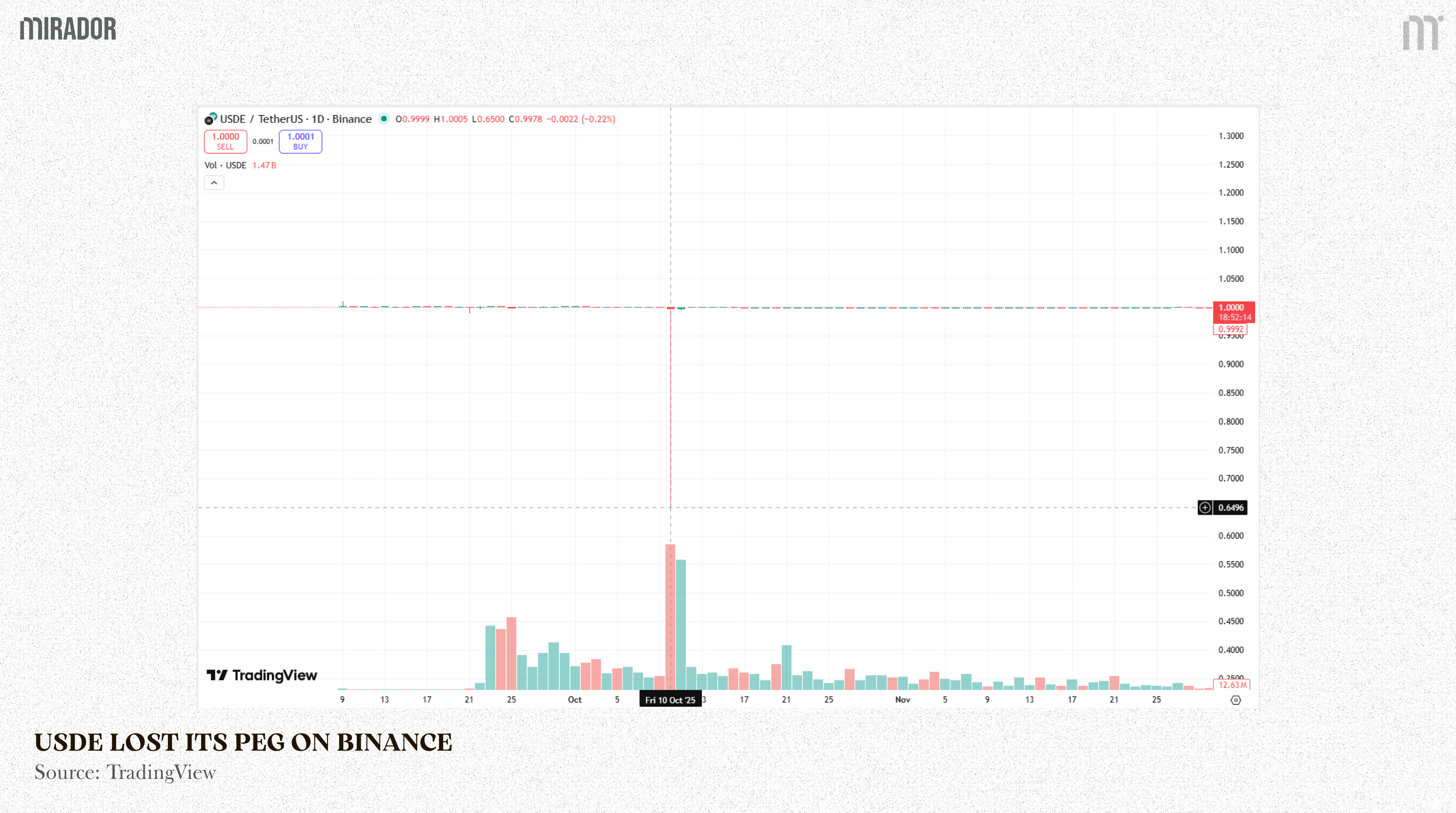

One of the biggest concerns for traders when deciding whether to trade on HyENA is the risk of losing the USDe’s peg.

USDE previously had a history of losing it peg. On 10/10, USDe price on Binance dropped to $0.65, causing many positions related to this stablecoin to be liquidated.

However, as stated by Guy Young, founder of Ethena Labs, this was not due to problems with the collateral or Ethena itself, but a failure of the internal Binance oracle, which fetches data from its own orderbook rather than an external price feed.

Binance’s oracle design flaw was the major vulnerability and also the root cause in this case. On the same day, this CEX announced a promise to switch to external price sources by October 14.

About the risk of depegging caused by the Ethena itself, USDe maintains its peg 1:1 via delta-hedging mechanism as mentioned above (i.e. long spot and short perps). Other than that, this mechanism also helps Ethena to earn positive funding rates from short perps, which is also Ethena’s revenue.

Certainly, the future is unpredictable, but since its launch in early 2024, USDe has not experienced any depegging incidents due to insolvency risks stemming from the protocol itself.

Oracle Risk

About perpetual contracts on HyENA, USDe is used only as collateral of maintenance margin, while the oracle price is still quoted in standard USD. By not converting USDe to USD in the oracle layer, HyENA cleanly separates pricing risk from collateral risk.

Price fluctuations in USDe on HyENA only affect the collateral asset class, impacting traders’ margin capacity rather than shaping market prices. Since USDe is not referenced in the oracle system and plays no role in calculating the reference price, oracle-induced price distortions cannot trigger or amplify USDe price breakouts. Therefore, the risk that USDe depegs due to the oracle price won’t exist.

Also, to power the trading infrastructure, HyENA perps are primarily fetched from Edge – oracle protocol of Chaos Labs to compute funding rates and is also a component of the mark price calculation. Unlike leading oracle providers like Chainlink or Pyth, Edge is a new decentralized oracle protocol just launched for over 2 months so it needs more time to test its security.

So, as a risk mitigation measure, HyENA is also running with a backup oracle provider as failsafe and will reuse oracle prices from Hyperliquid, which is a weighted median of CEX prices. For instance, the oracle price of BTC-USD perp on HyENA will match that of the BTC-USD perp on Hyperliquid.

In short, on HIP-3, a deployer has the full control over their oracle selection. While HyENA’s use of Chaos Labs’ oracle enables rapid deployment, the oracle’s limited track record in live perp markets introduces an additional risk factor that traders should be aware of.

If you are a risk-averse person, trading on HyENA HIP-3 should be taken into consideration. But vice versa, this perp DEX can be a suitable option for risk-takers.

CONCLUSION

Based on the analysis above, HyENA should not be viewed merely as another perp DEX on Hyperliquid, but as a real-world stress test for the HIP-3 framework and USDe-based margin design.

Its capital-efficient structure shows how perps can evolve beyond pure speculation into yield-generating infrastructure. Yet, this efficiency comes with new layers of risk - collateral stability and oracle reliability - that traders can no longer afford to ignore.

Whether HyENA becomes a blueprint for future HIP-3 deployments or a cautionary example will depend not on narrative, but on how these risks unfold in real market conditions.On the other hand, from the trading perspective, besides the profitability, traders also need to pay attention to some potential concerns related to the collateral’s depegging and oracle risk.

Disclaimer

This article is an independent educational analysis of HyENA and its deployment within the HIP-3 framework on Hyperliquid. Our goal is to help readers understand how HyENA’s capital-efficient design, USDe-based margin, and oracle dependencies function in practice, and from there, form their own perspective on the associated opportunities and risks.

All concepts are presented in a clear and approachable manner, without assuming deep prior knowledge of HIP-3 mechanics or advanced perpetual trading infrastructure. The content is provided for informational purposes only, and readers are encouraged to conduct their own research before engaging in any trading or DeFi activity.