INSIDE AAVE HORIZON: A THREE-PERSPECTIVE MECHANISM BREAKDOWN

AAVE Horizon - broken down through users, borrowers, and the issuer perspectives to reveal yield, risk controls, and core constraints.

INTRODUCTION

DeFi transactions settle quickly and protocol metrics update continuously. RWAs do not operate the same way. Real-world assets are not repriced every block, their valuations are typically published on a schedule (NAV reports), and their transferability can be restricted by compliance rules such as allowlists and settlement requirements.

Aave Labs’ Horizon (launched March 2025) combines these two systems in one lending market. The stablecoin side behaves like a normal on-chain money market. The RWA collateral side depends on off-chain custody, legal structures, and periodic valuation updates. Because these components update at different speeds and under different constraints, key DeFi expectations are not guaranteed. Withdrawals may be delayed by off-chain processes, liquidations may depend on stale or delayed valuations, and price inputs may reflect reported values rather than real-time market discovery.

This article analyzes Horizon as a mechanism. It focuses on how yield is generated and how collateral value is defined and maintained under these constraints.

KEY TAKEAWAYS

Section 1 : Stablecoin Supplier: Supplier yield = borrower interest, driven by utilization/rate model; incentives only adjust the displayed APY.

Section 2 : Borrower: Borrowing is allowlisted and NAV-priced; liquidations can be NAV-event-driven and collateral may be transfer-restricted.

Section 3 : Issuer/SPV/Custody: Collateral value comes from an off-chain NAV pipeline (issuer/SPV/custody → NAV → oracle).

OVERVIEW: WHAT HORIZON REALLY IS

Horizon is Aave’s RWA lending market: anyone can supply stablecoins, but only allowlisted institutions can borrow, because the collateral is permissioned tokenized (Real-World Asset tokens with transfer and access restrictions).

In the simplest terms:

Horizon is like a “DeFi bank”: deposit options are open to everyone, but collateral and borrowing options are only open to verified users.

HORIZON SPLITS THE MARKET INTO TWO HALVES.

The first half is RWA collateral. This side is controlled. Only institutions that have been approved and allowlisted by the issuer can supply RWA tokens as collateral.

The second half is stablecoin liquidity. This side is open. Regular users can supply stablecoins such as USDC and earn yield.

The intersection is borrowing. You can only borrow from the stablecoin pools if you are part of the group that has supplied valid RWA collateral.

We will explain more detail in next part, but totally, in plain terms, Horizon lets anyone deposit, but borrowing against RWA collateral is restricted to verified users.

So, from here on, we use borrowers to refer to allowlisted institutions that supply RWA collateral and borrow stablecoins from Horizon.

We use stablecoin suppliers to refer to users who deposit stablecoins (e.g., USDC) into the pool to provide liquidity and earn yield.

HOW HORIZON DIFFERS FROM A NORMAL AAVE MARKET

1) Collateral access is restricted

On Aave Core, most collateral is crypto-native (e.g., ETH, wBTC, major native tokens) and anyone can use it.

On Horizon, collateral is RWA ( e.g., VBILL, JAAA ) , so only approved participants can supply it.

2) Collateral price is NAV-based, not purely market-based

Aave Core collateral is typically priced by market-reflective feeds. ( “Market-reflective feeds” are price oracles that track prices formed in active markets (DEX/CEX) and update frequently based on real trading. In other words, the collateral price is tied to continuous market discovery, not periodic NAV-style reporting.)

Horizon RWAs often depend on NAV (Net Asset Value) updates reported by an issuer/NAV agent and published on-chain via an oracle. That means the system depends on an off-chain valuation and reporting cadence, not just on-chain trading.

3) RWA collateral positions may be non-transferable

To keep the market permissioned, the receipt token that represents an RWA collateral position can be made non-transferable. This means it can’t be freely sent or traded like a normal token. It’s not typical DeFi behavior, but it ensures the collateral position stays inside the allowlisted group and can’t be passed to unapproved wallets.

Overall, we use this diagram to summarize Horizon’s end-to-end flow before going into details.

Off-chain, an issuer creates the RWA token through an SPV (Special Purpose Vehicle) that legally owns the underlying assets, while a custodian holds and safekeeps those assets. A NAV provider produces valuation updates, and an oracle publishes NAV on-chain so the protocol has a usable collateral “price truth.”

On-chain, borrowers supply the RWA token as collateral and borrow stablecoins from the Horizon market. In parallel, suppliers can deposit liquidity permissionlessly and earn interest that is ultimately paid by borrowers. Governance and operations are split: Aave DAO sets risk limits, while Aave Labs coordinates day-to-day execution and partner operations.

To dive into Horizon’s internal mechanics, in the next section, we will analyze it through three perspectives: the stablecoin supplier, the borrower, and the RWA issuer. This approach helps readers understand how the system works end to end, where yields and risks actually come from, and which parts depend on on-chain logic versus off-chain processes.

SECTION 1 : PERSPECTIVE 1 - A STABLECOIN SUPPLIER

From a supplier’s view, Horizon feels like a normal Aave.

You supply USDC, receive an aToken, and see an APY on the screen. But the key point is simple: as a stablecoin supplier, you are not earning Treasury coupons. You are earning interest paid by borrowers, exactly like any lending pool.

So what should you actually watch?

Utilization (pool usage): if borrowing demand is low, your supplied liquidity sits idle and yield drops.

Borrow rates: when utilization rises, borrowers pay more, and that is what flows back to suppliers.

Liquidity on withdrawal: when you withdraw, you are withdrawing from the pool’s available liquidity, not from an SPV selling assets for you. If the pool is heavily utilized, withdrawals can feel tighter for the same reason they can on Aave.

Therefore, to better understand how interest is calculated, let’s break down exactly how stablecoin suppliers earn yield in Horizon.

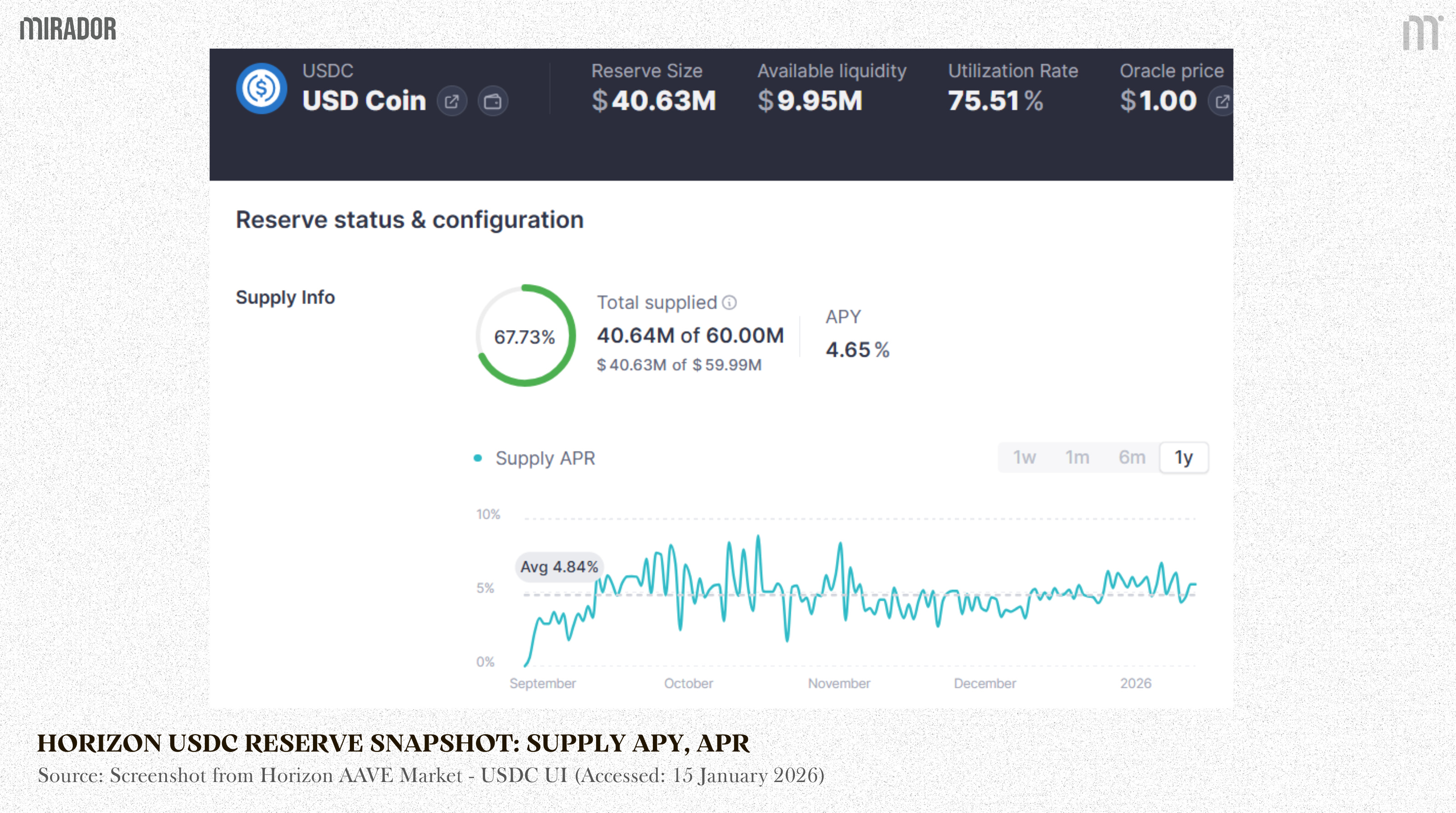

UTILIZATION

Utilization (U) measures how much of the supplied stablecoin liquidity is currently borrowed.

U = Total Borrowed / Total Supplied

Utilization over time for the Horizon USDC pool

Interest rates react to utilization through two operating zones on the rate curve:

Normal zone (below the kink): ~0% to ~90% utilization.

In this range, borrow rates rise gradually as utilization increases. In the chart, the pool’s Current U is 81.14%, which is still below the Optimal ~90%, so it is operating in the normal zone.Protection zone (above the kink): > ~90% utilization.

Once utilization moves past ~90%, borrow rates ramp up much faster (the curve steepens sharply). The goal is to protect remaining liquidity and push utilization back down by making borrowing more expensive.Kink / breakpoint: ~90% utilization on this chart.

This is the threshold where the interest-rate model switches from “gradual increase” to “aggressive increase.”

Because Horizon only allows allowlisted institutions to borrow, its utilization reflects borrowing demand from that restricted group—not from the broader user base.

When utilization rises, it means approved borrowers are actively borrowing stablecoins against their RWA collateral. Because Horizon only has a small, restricted set of borrowers, utilization can move sharply depending on when a few large borrowers borrow or repay, rather than changing smoothly with broad retail activity. When one or two large borrowers become active, add collateral, or receive updated NAV-based borrowing power, utilization can shift noticeably in a short period.

BORROW APY AND SUPPLY APY: THE REAL MECHANICS BEHIND THE NUMBERS

BORROW APY

Borrow APY (Annual Percentage Yield ) is the interest rate borrowers pay to the pool when they borrow USDC (or another stablecoin). It is not manually set by a team. It is the output of the pool’s interest-rate model, which reacts to how “tight” liquidity is.

When liquidity is abundant, borrowing is cheaper to encourage demand.

When liquidity becomes scarce (high utilization), borrowing gets more expensive to protect liquidity and rebalance the pool.

Borrow APY depends on Utilization

Where is the pool’s interest-rate curve (it increases as utilization rises).

SUPPLY APY

Supply APY is what suppliers earn for depositing USDC into the pool. The baseline source of supply yield is simple: borrowers pay interest, and suppliers receive a share of it.

Supply APY is usually lower than Borrow APY for two reasons:

Only the portion of liquidity that is actually borrowed generates interest (utilization matters).

The protocol keeps a portion of borrower interest as reserves (reserve factor).

This explains why numbers “make sense together.”

Example intuition: if borrow APY is ~7–8%, utilization is high, and reserve factor > 0, base supply can naturally land around ~5–6%.

HOW INTEREST ACCRUES IN HORIZON

Horizon records interest the same way Aave does: through aTokens (for suppliers) and debt tokens (for borrowers), not through manual interest payments.

If you supply: you receive an aToken that represents your deposit. Your yield accrues automatically through the aToken mechanics.

Example: supply VBILL => receive aHorRwaVBILL.

If you borrow: the protocol mints a debt token that represents what you owe. Your debt grows over time as interest accrues.

Example: borrow USDC => you receive USDC, and your USDC debt token balance increases over time.

APY AND APR

Aave’s UI can show both APR and APY, which is easy to confuse.

APR is a simple annual rate that does not include compounding, while APY is the effective annual rate after compounding.

In practice, Aave interest accrues continuously: lenders’ aTokens grow over time and borrowers’ debt grows over time. So the most accurate way to read the UI is: stablecoin suppliers earn Supply APY, and borrowers pay Borrow APY. If APR is also shown, treat it as a simplified, non-compounded version of the same rate.

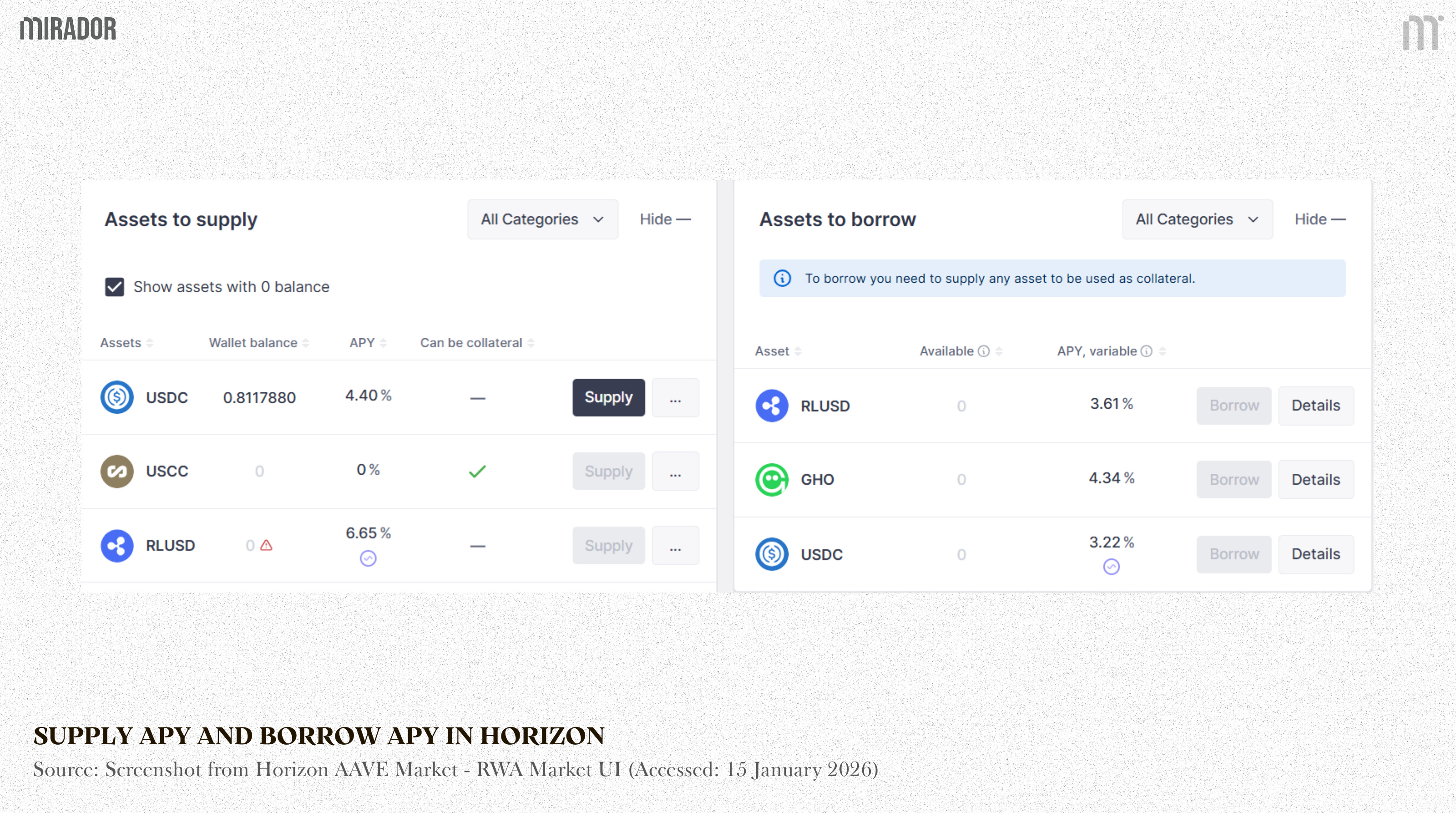

WHY THE UI CAN SHOW BORROW APY < SUPPLY APY ?

This is the confusing part. The interface can show different types of numbers for borrowing vs supplying because of incentives (rebates) such as Merkl.

Borrow: The UI may show the “net cost” after rebates

Borrow can have two layers:

Protocol Borrow APY: the raw interest rate produced by the pool

Borrow incentives (rebates): extra rewards for borrowers (e.g., via Merkl) that reduce the effective cost

Merkl incentives are third-party rewards designed to push specific behavior in the market, such as borrowing or supplying. They are separate from Horizon’s core lending engine: Merkl does not modify the pool’s protocol interest-rate curve or how interest accrues inside the pool. Instead, Merkl adds an external reward layer on top of the protocol rates. When borrowers receive incentives, their effective cost can be lower than the protocol borrow rate (because rewards offset part of the interest). When suppliers receive incentives, the APY shown on the interface can be higher than the base supply yield (because rewards are added on top)

So what the borrower effectively feels is:

Example : In the screenshot, the borrower’s effective rate is:

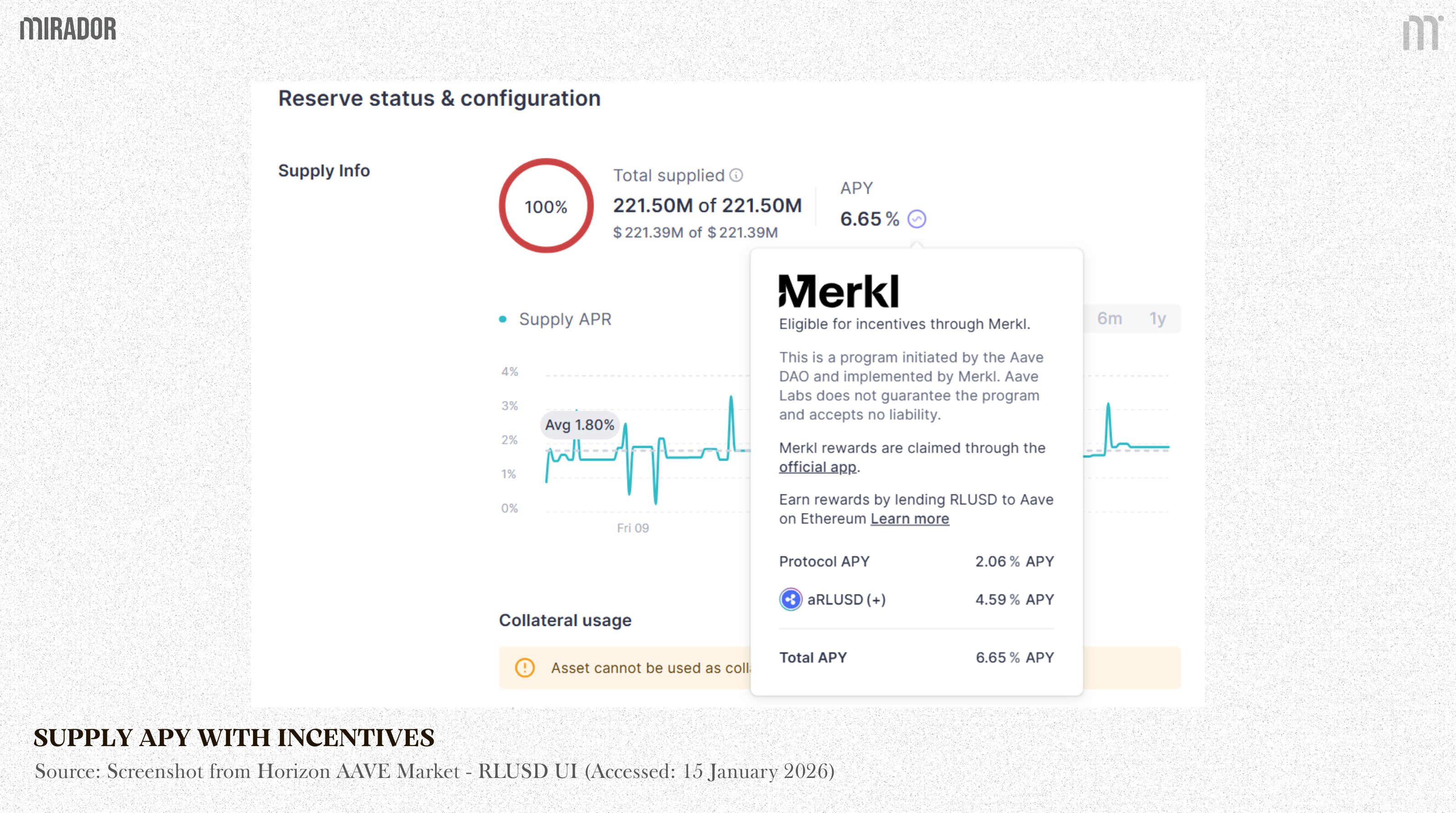

Supply: The UI may show “base + incentives”

Supply can also include incentives:

Base Supply APY: from borrower interest (the lending engine)

Supply incentives: extra rewards paid to suppliers (campaigns, subsidies, emissions)

So the displayed number may be:

Example : In the screenshot, the borrower’s effective rate is:

Therefore, Horizon’s APYs are not contradictory: the protocol sets borrow and supply rates through utilization and reserve factor, while Merkl incentives can rebate borrowers or boost suppliers. When Borrow APY looks lower than Supply APY on the UI, it’s usually because incentives are being mixed into the displayed numbers, not because the lending math is broken.

SECTION 2: PERSPECTIVE 2 – THE BORROWER

On the borrower side, Horizon is not a “supply and earn” product. It is a gated borrowing workflow. Institutions first go through onboarding steps such as KYC (Know Your Customer - identity verification), legal agreements, issuer approval, and allowlisting (being added to an approved-access list).

Only after that can they deposit permissioned RWA token as collateral and borrow stablecoins from the pool.

Once collateral is deposited, the position follows the same lending risk logic as Aave, but the key inputs behave differently. Borrowing power is defined by LTV (Loan-to-Value, the maximum borrowable percentage of collateral value) and liquidation thresholds (the point where a position becomes eligible for liquidation).

The difference is the collateral “price.” For many RWAs, value is not discovered on a DEX in real time. It is driven by NAV (Net Asset Value, the reported per-token value of the off-chain asset portfolio) updates that are produced off-chain and then published on-chain.

So the next step is to break down the borrower mechanics that actually move Horizon’s risk: how LTV is set, adjusted and what events push a position toward liquidation (forced debt repayment + collateral seizure).

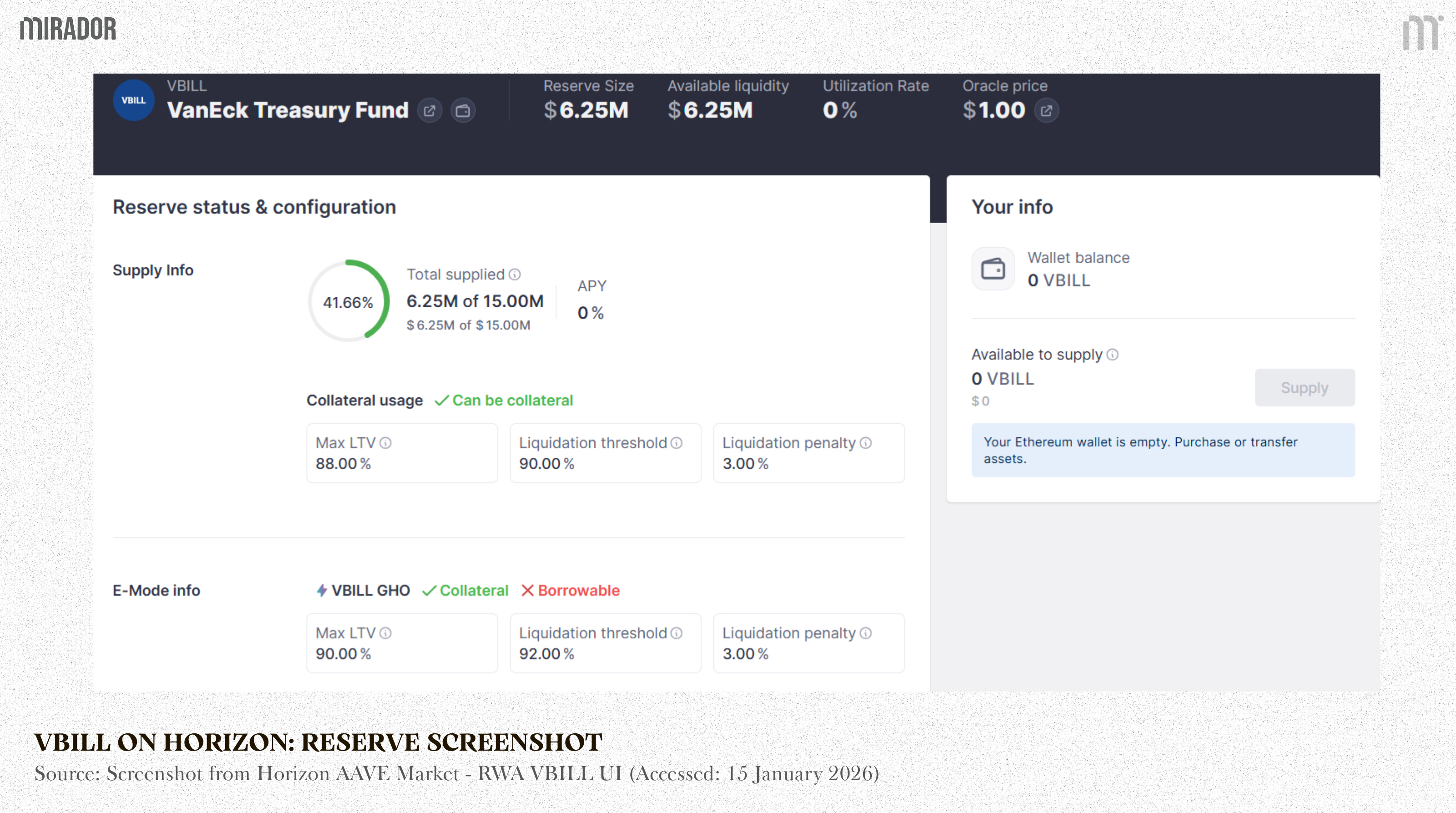

LTV ( LOAN-TO-VALUE)

In Horizon, the borrower (an allowlisted institution) starts by depositing an RWA token as collateral and then borrowing stablecoins. That is why LTV is one of the first parameters that matters on the borrower side.

LTV in Horizon is not calculated differently from Aave Core. It is the same concept and the same basic logic: maximum borrowable value as a percentage of the collateral value.

Max LTV is the initial borrowing cap: at position opening, it defines how much the borrower can borrow relative to the collateral’s value (as determined by the oracle price, which usually reflects the latest NAV update).

Example

VBILL shows Max LTV = 88% , Oracle price = $1.00. If an allowlisted borrower deposits VBILL worth $10,000, the maximum initial borrow is approximately:

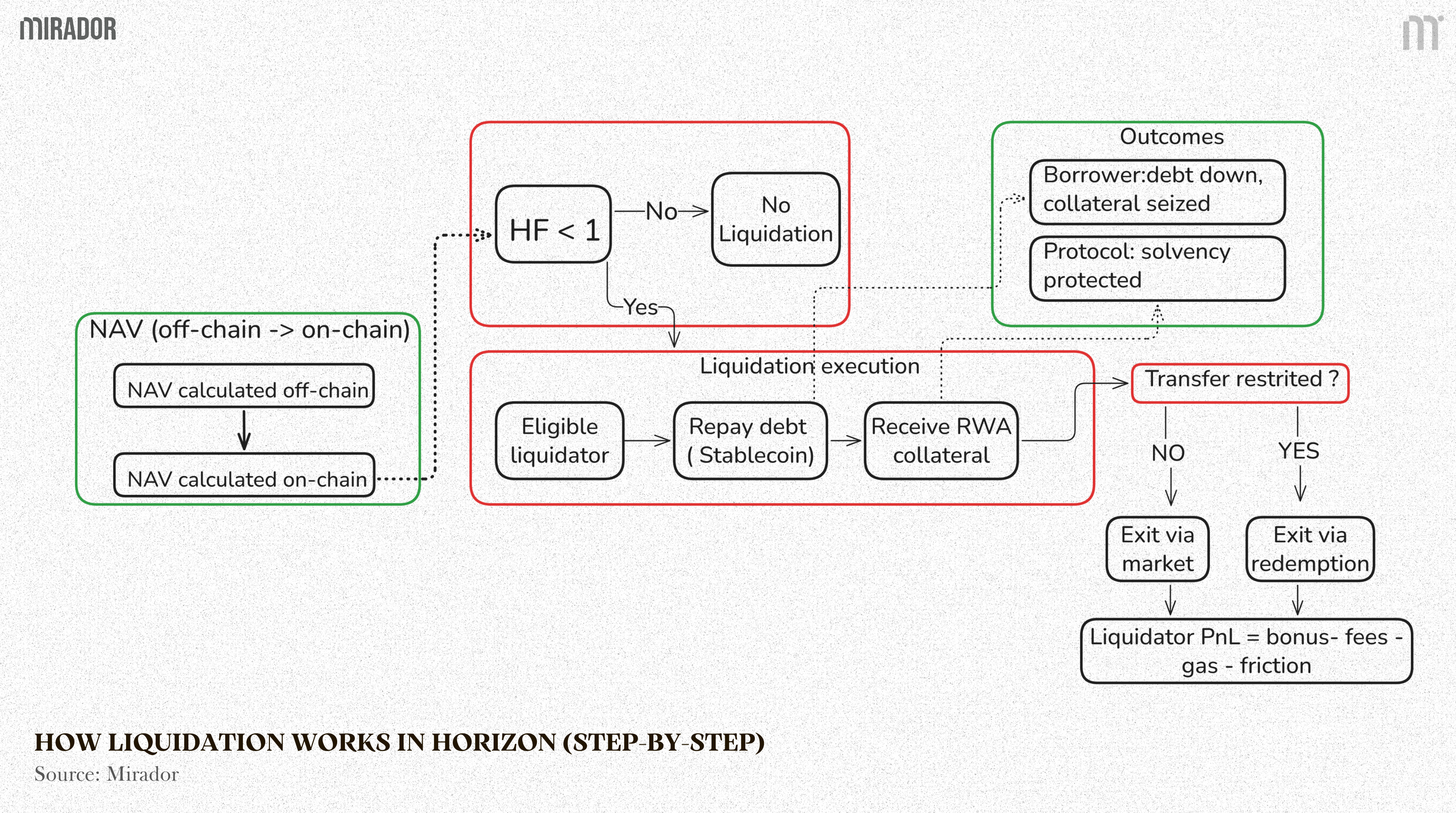

LIQUIDATION IN HORIZON: SAME TRIGGER, DIFFERENT CONSTRAINTS

After LTV, the next borrower-side mechanism that matters is liquidation. Horizon uses Aave’s standard risk logic, but the inputs and constraints are different.

1) The trigger is the same: health factor below threshold

In both Aave Core and Horizon, a position becomes liquidatable when its health factor falls below the liquidation threshold. This can happen because:

Debt grows over time from interest, or

Collateral value drops (in Horizon, this is often driven by NAV updates rather than real-time market prices).

2) The key difference is “price truth”

Aave Core (crypto collateral): collateral pricing is market-reflective and updates frequently via oracles that follow active trading venues. Health factor moves continuously with the market.

Horizon (RWA collateral): many collateral types are valued using NAV updates that are computed off-chain and then published on-chain. That changes liquidation dynamics:

A position can look healthy under the previous NAV, then become liquidatable immediately after a new NAV is posted.

The dominant risk is not normal volatility; it is bad NAV reaching the chain (late, incorrect, or outlier values).

3) Execution is more constrained because collateral may be permissioned

In standard DeFi liquidation, collateral is typically a freely transferable ERC-20, so the loop is simple: liquidator repays debt → receives collateral → sells on a DEX → recovers liquidity.

In Horizon, RWA collateral (or its receipt token) can be transfer-restricted for compliance. Practical implications:

Not every address can liquidate or receive collateral. Liquidators may need to be eligible/allowlisted.

Even after receiving collateral, the liquidator may not be able to “dump” it immediately on a DEX. Exit may depend on restricted venues, redemption flows, or off-chain processes.

4) Who gains and who loses in liquidation (economic clarity)

Borrower (loses): collateral is taken at a discount relative to the repaid debt. This is the effective liquidation penalty. The borrower benefits only in one sense: their debt is reduced, preventing the position from becoming insolvent.

Liquidator (gains): earns the liquidation bonus (collateral received worth more than the debt repaid), but takes on additional constraints (eligibility, exit friction, operational risk).

Protocol / lenders (benefit): liquidation’s purpose is solvency protection—it prevents bad debt and protects suppliers. The protocol’s “gain” is risk containment and system stability, not necessarily direct profit.

So, we can see overall liquidation process through this diagram :

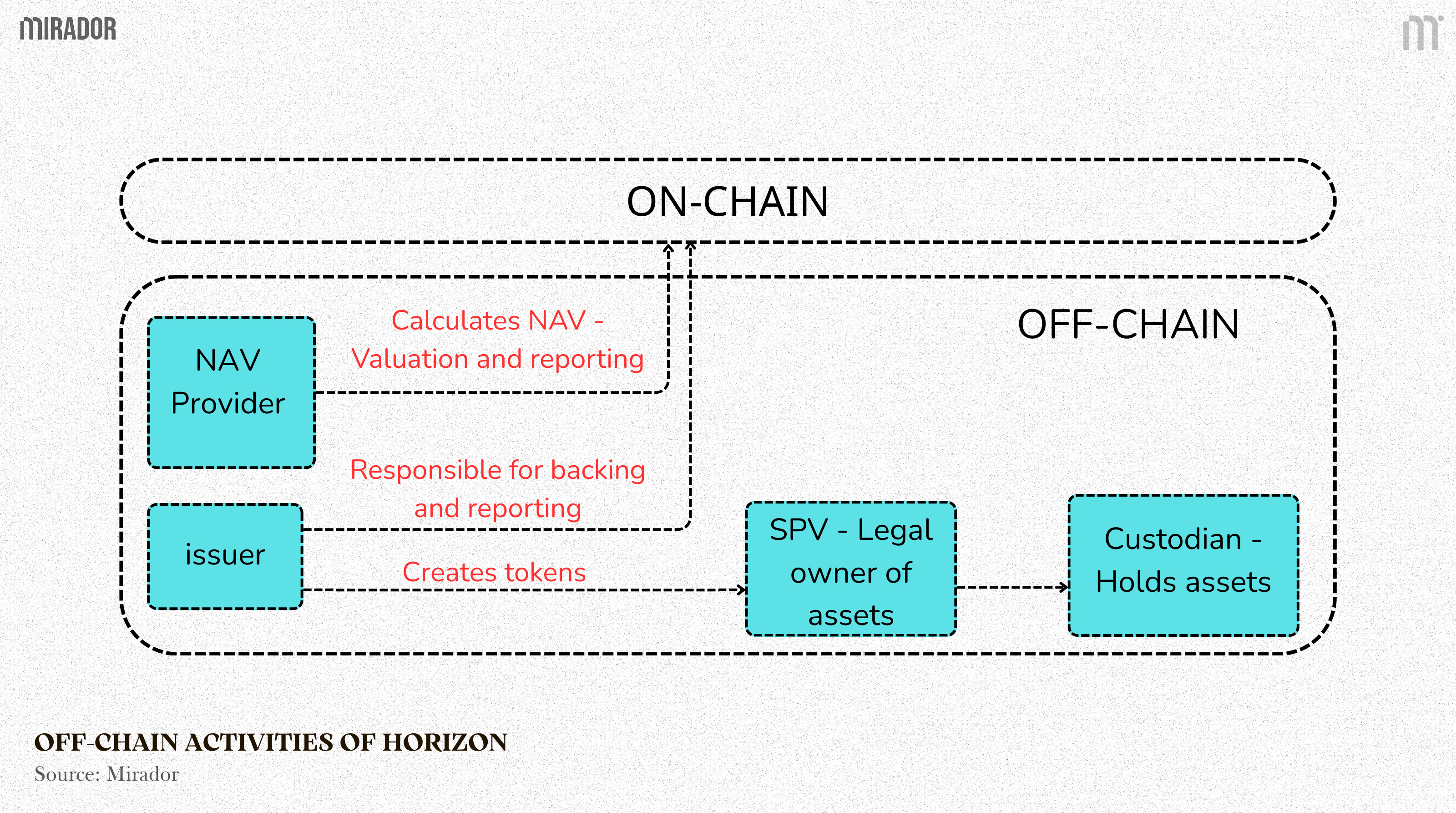

SECTION 3 : PERSPECTIVE 3 - THE ISSUER, SPV, AND CUSTODY STACK

This is the part the interface does not show you.

Off-chain roles (high level):

Issuer : designs the product, sets eligibility rules (allowlist/whitelist), and is responsible for ensuring the token is backed by legally owned assets.

SPV (Special Purpose Vehicle): the legal entity that owns the underlying assets. It is typically structured to be bankruptcy-remote so the assets are ring-fenced from the issuer’s balance sheet.

Custodian (custodian): the regulated safekeeping layer that actually holds the instruments (T-bills, cash, credit positions) and handles settlement and segregation.

NAV provider (NAV calculation agent): produces valuation reports for the portfolio on a defined schedule and methodology.

Oracle : publishes the NAV value on-chain so the protocol can use it as the collateral reference price.

NAV IS THE COLLATERAL PRICE, BUT IT UPDATES ON A SCHEDULE

RWA collateral in Horizon is often priced by NAV, not by continuous on-chain market discovery. At a high level:

Where:

AUM (Assets Under Management): total market value of what the SPV/fund holds (cash, T-bills, bonds, short-duration notes, private credit).

Fees: costs charged at the structure level (management, custody, audit, admin).

Liabilities: unpaid expenses or other obligations at the vehicle level.

Tokens outstanding: total RWA token supply currently in circulation on-chain.

Two pricing systems run in parallel

Horizon runs two “clocks” at the same time:

NAV prices the RWA collateral side on a reporting cadence.

The Aave interest-rate model prices stablecoin borrowing in near real time based on utilization.

These two clocks can move at different speeds, which is why the market can look normal on the lending side while the collateral side is operating on periodic updates.

NAV APY is not the supplier’s yield

NAV APY is just an annualized view of NAV movement. It describes the RWA portfolio performance, not what stablecoin suppliers earn. Supplier yield still depends on borrowing activity and the lending engine.

The key risk to track

The main failure mode is bad NAV reaching the chain (late, wrong, or outlier). If the protocol consumes incorrect NAV, it can misprice collateral and trigger incorrect risk outcomes. This is why RWA markets rely on validation, bounds, and emergency controls around NAV publishing.

NAV is an off-chain number, so the protocol cannot “verify” it using on-chain data alone. Instead, RWA markets reduce NAV risk through a controlled publishing process and strict guardrails. Off-chain, NAV is typically calculated and reconciled against custodian statements (often with a fund admin/attestation layer). On-chain, the protocol only accepts NAV updates from authorized signers, and it applies validation rules such as freshness checks (reject stale NAV), deviation bounds (reject large jumps vs. the last NAV), and outlier filters. If an update looks abnormal, emergency controls (pause/freeze) can temporarily stop borrowing or liquidation to prevent mispricing from causing incorrect risk outcomes

A quick example:

A fund holds $2,000 of T-bills and mints 2,000 tokens. NAV starts at 1.00.

After interest accrues, the portfolio becomes $2,010. The new NAV is:

No new tokens are minted. Value increases because each token becomes worth more.

CONCLUSION

We see Horizon as Aave’s attempt to integrate RWAs into a lending market in a way that can work operationally, using permissioned collateral and NAV-based valuation alongside open stablecoin liquidity.

Whether it succeeds is less about the APYs and more about execution quality: the reliability of the off-chain NAV pipeline, the clarity of intervention boundaries, and how these constraints affect liquidity, liquidations, and user expectations under stress.

DISCLAIMER:

This article is intended as a conceptual and educational breakdown of Aave Horizon’s RWA lending design. The focus is on mechanism-level intuition, how rates, utilization, collateral valuation, and liquidation constraints work rather than exhaustive smart contract implementation details.

It is structured as a three-perspective framework (stablecoin supplier, allowlisted borrower, and issuer/SPV/custody) to clarify which parts are on-chain logic versus off-chain operations. A deeper contract-level walkthrough and transaction-level proofs can be presented separately in a follow-up part.